In 2004 the IRS clarified, through private-letter rulings, that a trustee or custodian who purchases shares of a gold exchange-traded fund for an IRA is not treated as acquiring a collectible, so the transaction does not trigger a taxable distribution to the account owner. Because the purchase relies on this legal exception, the shares can be owned by a traditional IRA without the owner holding physical gold. The position is deemed a paper investment held inside the regular IRA structure. As a result, gold ETF shares can be bought, sold, and traded within the account without immediate tax consequences, provided the IRA custodian - not the individual owner - maintains custody of the grantor-trust structure that underlies most gold ETFs.

Can you hold gold ETFs in an IRA?

Yes, you can hold gold ETFs in an IRA. An IRA is free to purchase shares of a gold ETF because the security is classified as a grantor investment trust, an asset class that IRA owners can hold without triggering a prohibited-transaction rule. The same rule applies to silver ETFs and to funds that buy mining stocks. The IRA buys the mutual-fund or trust shares, not the metal itself, so no physical gold or silver is ever taken into the account.

Can I hold a gold ETF in a Roth IRA?

Yes, you can hold a golf ETF in a Roth IRA. A regular Roth IRA allows you to hold traditional assets like stocks, bonds, mutual funds, and exchange traded funds, so a gold ETF is automatically permitted. Because the shares are classified as securities, you can buy gold in a Roth IRA without needing a special self-directed custodian. Any brokerage that offers Roth accounts can add the position. SEP IRAs can invest in the same assets as standard Roth or Traditional IRAs, which plainly includes exchange traded funds. Whether your plan is a Roth IRA or a SEP IRA, you can track the price of bullion through a gold ETF while staying inside the familiar IRA framework.

Physical gold is a primary option for investing in gold through a Roth IRA, but it is not the only one. Gold IRAs are set up as Roth IRAs, yet those vehicles are distinct from the everyday Roth you open at a mainstream broker. They require a self-directed custodian and limit you to approved coins like American Gold Eagles or Canadian Maple Leafs. A gold ETF can live in the same brokerage Roth IRA that already contains your other funds, so you avoid extra paperwork and annual storage fees while still gaining exposure to bullion prices. SEP IRA holders enjoy identical freedom, because the SEP can invest in all the same assets as your standard Roth or Traditional IRA. Keep in mind that Roth contributions are made with after-tax dollars, so once the ETF shares are inside the account any future appreciation and eventual qualified withdrawals will be tax-free, the same advantage that applies to any Roth holding.

I investigated and confirmed that maintaining a precious-metal ETF inside a Roth IRA is permitted. I contacted my IRA custodian, and the procedure was easy: the custodian simply buys the chosen ETF shares within my account. Any increase in the price of the ETF will be tax-free upon withdrawal in retirement, a long-term, tax-free growth prospect that is exactly why I opted for a Roth IRA.

Thomas GoldfreburgInvestor at Goldfreed

What is the difference between a gold ETF and a gold IRA?

A gold ETF is an exchange-traded fund that trades like a stock on exchanges, offering exposure to gold's price without direct ownership of the metal. It tracks the gold price through shares that closely mirror the current gold spot price, and it can be bought or sold instantly during market hours. Because ETF shares do not entitle the investor to any amount of physical gold, the fund holds physical gold in secure vaults, yet the investor holds only a paper-based asset. Gold ETFs provide lower entry costs, lower management fees, high liquidity, and convenience. They avoid storage or insurance costs and allow buying or selling quickly without restrictions. Transaction costs for gold ETFs are generally lower than buying physical gold, and the expense ratio - often about 0.15% per $10,000 invested - covers management and administrative costs, meaning the ETF investor will lose a small percentage of the investment's value each year to this fee.

A gold IRA is a self-directed retirement account that holds physical gold coins or bars approved by the IRS. Gold IRAs involve additional costs and fees compared to a physical gold ETF, including storage fees, insurance, and custodian charges, making them less liquid and more expensive to maintain. While both vehicles provide exposure to gold's price movements, gold IRAs and gold ETFs differ in how they're taxed, stored, and managed. Within a traditional gold IRA, growth is tax-deferred, yet withdrawals are taxed as ordinary income, potentially at a lower rate in retirement. Clear documentation and secure vault storage prove ownership of the metal, but the investor cannot take personal possession without triggering a taxable distribution. The right gold investment choice depends on your goals and timeline: gold ETFs offer a short-term, high-liquidity option with lower fees, whereas gold IRAs serve long-term retirement savers willing to accept higher costs for the security of tangible metal within a tax-advantaged structure.

A gold ETF and a gold IRA diverge in form, access, and purpose. When I bought stocks of a precious metal ETF, I did not hold a direct right to any material bullion. Instead, I owned paper shares whose value mirrors the metal cost. I valued the ease of purchasing and trading through my definitive securities firm relationship, and I could observe the cost variations throughout the commerce hour. However, the ETF could not duplicate long-term protection. Seeking tangible security, I subsequently created a self-directed Gold IRA and maintained allotted, IRS-approved tangible precious metal in a protected strongroom. I bought physical precious metal coins, and this provided less liquidity likened to the ETF, the procedure needed an authorized bank to stow the physical precious metal coins I bought and a technical steward to handle the account, initiating administrative fixed charge. Despite the extra steps, I wanted physical protection, and the psychological advantage was substantial, for I got a deep feel of long-term safety that paper shares never supplied.

Thomas GoldfreburgInvestor at Goldfreed

What is a gold IRA rollover?

A gold IRA rollover is the process of transferring a portion of an existing retirement account into physical gold coins or bullion bars. The procedure can be carried out as a direct rollover, which sends money straight to the new custodian and avoids taxes and penalties, or as an indirect rollover, which gives you cash first but requires redeposit within 60 days to preserve tax-deferred status. Because the IRS limits taxpayers to one IRA-to-IRA rollover in any 12-month period, most investors favor the more straightforward direct option. Moving your IRA to gold offers a way to gain exposure to precious metals and diversify your retirement portfolio, and gold has historically served as a hedge against inflation, currency depreciation, and market volatility. A rollover protects savings from market swings because gold and precious metals hold their value in tough times, yet eligibility for any distribution must first be confirmed with the plan administrator. Once the transfer occurs under the management of a new custodian, the metals must be stored in an IRS-approved depository like Delaware Depository or Brinks Global Services, where insurance coverage and secure supervision are provided.

How to transfer 401k to gold IRA?

To transfer 401k to a gold IRA, a direct rollover is the more straightforward option: it avoids withholding taxes, prevents income taxes, and eliminates tax-penalty risk because it does not involve a check and does not require you to handle the money yourself. You can alternatively choose an indirect rollover, but this approach gives you cash first and comes with more rules: you must deposit the withdrawal within 60 days to avoid taxes and penalties. Whether you choose the direct or indirect route, the plan administrator must provide written notice informing you of your rights to roll over or transfer any eligible distribution of $200 or more and must facilitate the direct transfer to another plan or IRA without withholding taxes. A financial advisor or a Fidelity representative can guide you through the rollover process and help you consolidate old 401(k) accounts into a single gold IRA without taxes or penalties.

I conducted an investigation to choose an organization with a reputable track history, clear fee structures, and favorable consumer response. After selecting a respected precious metal IRA steward, I created a self-directed IRA account to serve as the end for my retirement money. I finished the needed paperwork to establish the account and supplied the custodian with the required details. Next, I communicated with the 401(k) manager and inquired about forms to arrange a trustee-to-trustee transfer, guaranteeing the money proceeded immediately between financial organizations. Once the immediate move was pushed from the old employer's 401(k) program administrator to the current precious metal IRA conservator, I told the gold IRA guardian to buy IRS-approved precious metal coins and bars, which were then put into a protected, insured facility.

Thomas GoldfreburgInvestor at Goldfreed

How to convert an IRA to gold?

To convert IRA to gold follow the steps explained below.

- Convert IRA into gold through a rollover

- Convert stocks into gold via self-directed IRA

- Start by selecting a trusted custodian who specializes in self-directed IRAs

- Put physical gold into an IRA by having or opening a self-directed IRA

You can convert an IRA to gold through two options - rollover or transfer. A rollover is direct or indirect: a direct rollover sends money straight to the new account and avoids tax penalties, while an indirect rollover gives you cash first but must be completed within 60 days or else triggers tax penalties. Rollover is initiated by requesting a direct rollover from a traditional IRA, a SIMPLE IRA, or a Thrift Savings Plan. The same form is reported on Form 8606. After funds reach the self-directed IRA, you purchase gold or silver and the custodian stores the metal in an approved vault. Direct transfer avoids taxes and the entire sequence - finding a custodian, initiating a rollover, purchasing metals - lets you convert stocks into gold via self-directed IRA without taking cash into your hands.

What are the tax rules for a gold IRA?

Traditional Gold IRA contributions grow on a tax-deferred basis and are tax deductible in the year you make them, with the exact deduction depending on your income level and participation in an employer-sponsored retirement plan. Roth IRA contributions are made with after-tax dollars so they do not provide an up-front deduction. Because the account is treated as an IRA rather than a personal holding of collectibles, you sidestep the 28% maximum collectibles tax that applies to gold purchased outside of retirement accounts.

Money that remains inside the gold IRA is not taxed while it compounds, yet whatever you withdraw is subject to ordinary income tax when distributed. Traditional IRA withdrawals are taxed as income, whereas Roth withdrawals are tax-free if qualified. Because of the IRA structure, investment in collectibles for IRA purposes are not subject to the 28% tax.

Early withdrawals taken before age 59 are subject to an extra tax of 10% in addition to ordinary income tax, and losses on these withdrawals are typically not deductible. Your IRA company will report each distribution to the IRS. If you wait until retirement to take the money out, you typically owe tax at that time, and if you are in a lower tax bracket then, the ultimate bite will be smaller.

Tax regulations regulating a precious IRA require precise attention to detail, because a single blunder could lead to substantial penalties and taxes or even spark a dispersion. Severe adherence to IRS rules affects the purity criteria of the metallic element and mandates that the precious metal be stored in an IRS-approved facility. I understand the tax-deferred growth: the total amount of my asset compounds over duration, yet holding fixed costs and policy prices decrease my total returns. I must recognize the absence of a direct authority over the tangible resource, because getting physical ownership of the precious metal myself could initiate a distribution, and the whole sum is then assessed as ordinary earnings at my maximum tax bracket.

Thomas GoldfreburgInvestor at Goldfreed

Can you withdraw from a gold IRA?

Yes, you can withdraw from a gold IRA. You can take distributions from your SEP-IRA or SIMPLE-IRA at any time, and the same freedom applies to a gold IRA. The process of withdrawing funds out of a retirement account is called taking a distribution, and a distribution is made in cash or in the form of the precious-metal holdings themselves. Cash distribution allows receipt of proceeds in cash, while taking physical possession of gold is treated as a withdrawal by the IRS. In either case, your IRA custodian will report the transaction to the IRS, and you will need to show the amount of the IRA withdrawal on Form 1040.

Withdrawal before age 59 is subject to 10% additional tax, and traditional IRA early withdrawals are assessed a 10% penalty unless an exception applies. Taxes on withdrawals are based on fair market value, so you will be liable for any taxes and penalties. After age 59 the 10% penalty disappears, yet ordinary income tax is still due. Beginning at age 73, RMD dictates the annual withdrawal amount, forcing a minimum distribution each year. You can liquidate the metal or request shipment of coins and bars, but physical possession of gold from a gold IRA is treated as a withdrawal, and the IRS will assess a 10% penalty for early distribution from qualified retirement plans if you are under 59 .

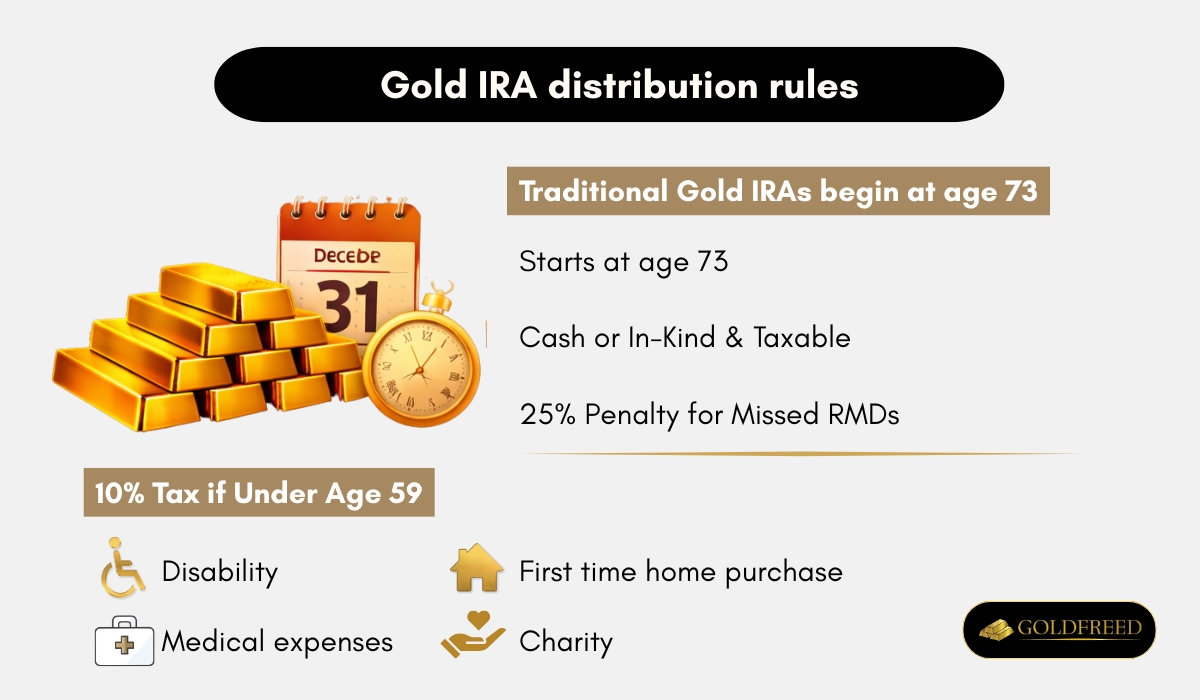

What are the rules for gold IRA distribution?

Under IRS rules, you must begin taking required minimum distributions from a traditional gold IRA at age 73 (as of 2024). Distributions are taken in cash or in-kind, and will be includible in taxable income. Your distribution is subject to a 10% additional tax if you are under age 59, unless you meet exceptions like disability, first-time home purchase, or qualified medical expenses. There is no need to show a hardship to take a distribution, and distributions are taken after age 59.

If you skip an RMD or do not take enough, the IRS charges you with a 25% penalty on the amount you were required to withdraw. RMD amount is calculated based on account balance and life expectancy factor using your IRA account balance as of December 31 of the prior year. Breaking RMD rules triggers immediate taxation and penalties on your entire account. Roth Gold IRAs do not require RMDs during lifetime, whereas surviving spouses can treat an inherited gold IRA as their own IRA.

Non-spouse beneficiaries must empty the account within 10 years. Qualified charitable distribution is an otherwise taxable distribution from a traditional IRA owned by an individual who is age 70 or over that is paid directly from the IRA to a qualified charity. Distributions are made in cash or in-kind in accordance with IRS guidelines, and in-kind distribution results in receipt of physical coins or other precious metals products. Precious metals must remain stored in secure independent insured storage facilities, and the organizations you pick as custodians and depositories affect your compliance.

What is the annual limit for a gold IRA?

For 2025, the annual limit for a gold IRA is $7,000. If you are 50 or older, you can contribute an additional $1,000, bringing the 2025 limit to $8,000.

These dollar caps apply to the combined total you put into all traditional and Roth IRAs you own. They are not separate for each account. Rollover money is not counted against these limits, and there is no dollar cap on how much you can roll over or transfer between IRAs, although you are limited to one IRA-to-IRA transfer per year.

What are the regulations for gold in an IRA?

The Internal Revenue Code treats gold and other precious metals as collectibles, so they are allowed inside an IRA only when strict standards are met. Gold must be at least 99.5% pure (.995 fineness), silver must be 99.9% pure, and platinum and palladium must each be 99.95% pure. The only exception is the American Gold Eagle coin, which is approved despite its 91.67% purity. Acceptable coins include government-minted American Eagles, Canadian Maple Leafs, Austrian Philharmonics, British Britannia (2013 and newer), Australian Kangaroo/Nugget and Lunar Series bullion coins, Chinese Pandas, and approved bullion rounds. Bars and rounds must be produced by an accredited refiner/assayer/manufacturer listed by a national mint or COMEX/NYMEX-approved source and must carry proper assayer certification.

Physical possession is strictly regulated: the metals are not held by the IRA owner. Gold must be stored in an IRS-approved depository - a licensed bank or an IRS-approved non-bank trustee - and the self-directed IRA custodian must arrange secure storage in that licensed depository. Home storage, private safes, or local safe-deposit boxes are prohibited, and any violation is treated as an immediate taxable distribution.

What are the best gold IRA ETFs?

The best gold IRA ETF is iShares Gold Trust Micro (IAUM) for investors who want physically backed exposure at the lowest possible cost. Its expense ratio of 0.09% is the lowest in the group, and assets under management sit at roughly $5.5 billion. SPDR Gold MiniShares Trust (GLDM) offers a similar low-fee profile while adding the liquidity that comes from a 30-day median bid-ask spread of 0.02%. Franklin Responsibly Sourced Gold ETF (FGDL) has generated the best one-year return at 45.04%, although its expense ratio of 0.15% is modestly higher and daily volume is thinner, so it is best suited to buy-and-hold owners who care more about performance than intraday trading flexibility.

SPDR Gold Shares (GLD) remains the most liquid pool for large or frequent trades: $137.0 billion in assets, a 0.01% bid-ask spread, daily volume of 2.6 million shares, and the most active options chain. iShares Gold Trust (IAU) is almost identical to GLD in tracking the LBMA Gold Price, but the 0.25% expense ratio makes it slightly more expensive. The fund still provides ample liquidity for most IRA owners, with $63.9 billion in assets and a 0.03% spread. Traders who prefer bullion stored in London contemplate Goldman Sachs Physical Gold ETF (AAAU), which keeps fees at 0.18% and holds $23.1 billion in metal.

Miners-focused ETFs like VanEck Gold Miners (GDX) and VanEck Junior Gold Miners (GDXJ) are available, but their 0.51% expense ratios and higher volatility make them complementary rather than core holdings inside a tax-advantaged retirement account. In practice, most IRA owners combine a low-cost physical ETF - IAUM or GLDM - for the core position with a smaller satellite in GLD when they need extra liquidity for rebalancing or required distributions.

How can I sell gold in my IRA?

You can sell the gold or precious metals in your IRA at any time without any taxes or penalties, provided you do not take the cash out of your IRA. The first step is to contact your custodian, because your IRA custodian facilitates the sale and you must follow their specific liquidation procedures. In most cases you will complete an Investment Direction form that tells the custodian what to sell and authorizes the transaction. The custodian then works with an authorized precious-metals dealer. You sell metals back to that dealer and the dealer issues an invoice on behalf of your IRA. Once the metals are shipped, the dealer wires the agreed buy-back amount and the proceeds are deposited into your IRA account, keeping the entire transaction inside the tax-advantaged wrapper.

If your metals are held in a self-directed IRA, you can liquidate precious metals any day the market is open, and you will repeat the process whenever you wish to rebalance or raise cash for other IRA investments. For owners of a home-storage gold IRA who need help, Certified Gold Exchange can coordinate the sale quickly. STRATA, like many custodians, does not buy or sell metals itself, but it and similar trustees will release the metal to an approved third-party dealer once the paperwork is in order.

My custodian conducted the selling at the current market cost on my behalf. The payoffs from the trade were put back into my IRA, so the currency stayed within the tax-advantaged refuge of the retirement account. The deals obeyed IRS rules for retirement accounts and the reallocation performed did not spark taxes.

Thomas GoldfreburgInvestor at Goldfreed

Expert behind this article

Thomas Goldfreburg

Thomas Goldfreburg is a gold investment advisor, author and founder of Goldfreed. Thomas's expertise is built on an academic foundation of a Bachelor of Science in Economics from Stanford University and complemented by market experience. Thomas specializes in gold IRA, ETF, 401k, and physical gold investments.