Investors generally suggest some allocation to gold because the metal provides diversification benefits and has low correlation with stocks and bonds. Financial institutions frame specific weights: Morgan Stanley CIO Michael Wilson proposes a 60/20/20 portfolio with 20 percent allocated to gold, while Morningstar's Role-in-Portfolio framework recommends individual investors limit gold exposure to 15 percent of assets or less. Ray Dalio endorses at least a 10 percent weight, and other practitioners argue that 10 percent to physical gold and 0-5 percent to gold-related equities strike a reasonable balance. Schoffstall said investors would be well positioned with a 5 to 15 percent allocation to physical gold and silver. Physical gold has the potential to provide solid returns and diversification, so every investment strategy includes a deliberate, disciplined allocation to the metal.

How much of your investment portfolio should be in gold?

Financial advisors recommend keeping a maximum of 5-10 % of your portfolio in gold, and investors with considerable allocations to gold don't generally hold more than 5 percent. This amount has a robust liquidity and historic resilience makes it a valued asset during times of economic stress. Alternative assets, including gold, therefore comprise no more than 5-10 % of a diversified investment portfolio.

Ray Dalio recommends allocating at least 10% of a portfolio to gold, while Wilson stated investors must contemplate swapping half of the bond portfolio for gold. Younger investors have higher suggested allocations, up to 15 %. Morningstar defines limited gold exposure as 15 % of assets or less and recommends individual investors keep gold exposure limited.

A five-to-ten percent allocation to precious metal is a reasonable extent for most stockholders seeking a proportion large enough to deliver diversification advantages and to act as an efficient counterbalance to paper investments, yet modest enough that it does not meaningfully drag on total portfolio growth during extended bull markets. I began my own excursion with a cautious two-percent stance, treating the tiny position as sensible insurance against intense industry unpredictability. The size stayed deliberately limited because I remained careful about over-allocating to a non-yielding asset. That small slice provided measurable benefits: I detected its low correlation with mainstream holdings during business downswings, and the mere presence of the metal delivered a measure of mental relief whenever economic uncertainness surfaced. My admiration for its protective function has since intensified, even though I still hope never to depend upon the position. The experience has confirmed that, for most investors, a low-single-digit allocation is sufficient to capture the hedge without stifling long-term growth.

Thomas GoldfreburgInvestor at Goldfreed

What is the optimal gold investment allocation for annual income?

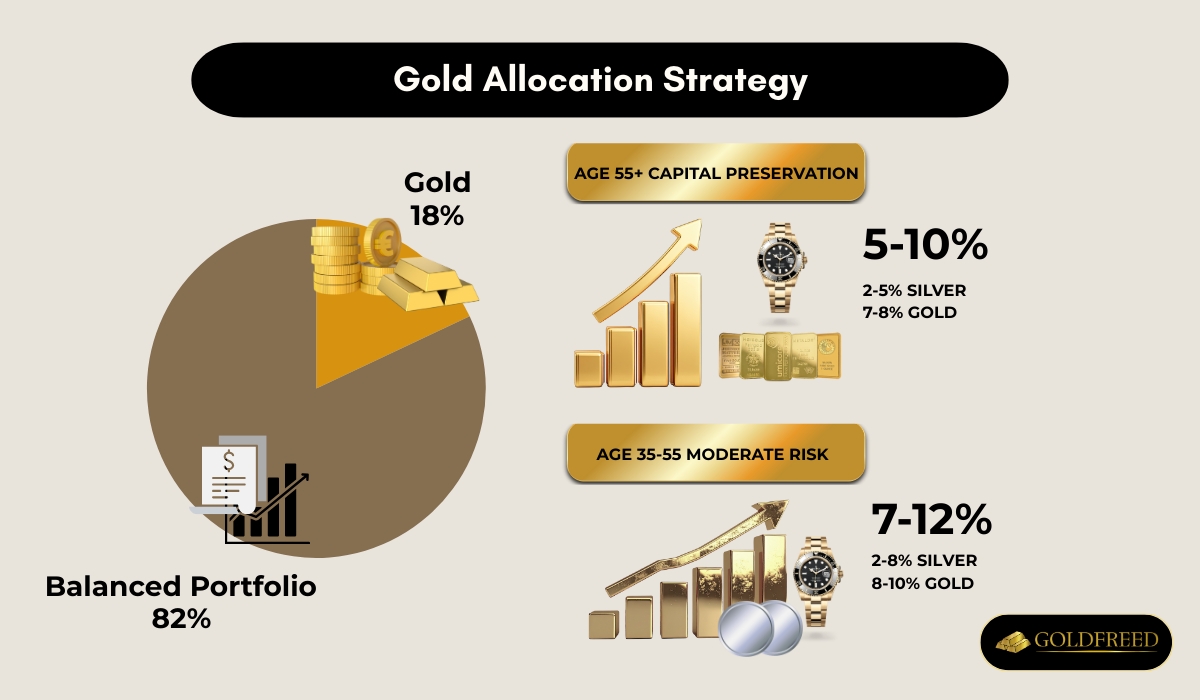

FPI's research shows that, from a risk-reward standpoint, the optimal allocation is 18 % in gold and 82 % in a balanced portfolio. This level boosted risk-adjusted returns across a wide range of allocation levels over the study period. Ray Dalio recommended 10% to 15%, while Jeffrey Gundlach suggested that an allocation of 25% is not excessive, and Alan demonstrates that 25% is optimal. Most advisors deem 25 % aggressive, yet it suits younger investors with high risk tolerance who target higher annual income potential through capital gains rather than dividends, because gold pays no dividends or interest.

For investors over 55 or those prioritizing capital preservation, experts recommend a 5-10 % total precious metals allocation. Investors aged 35-55 with moderate risk tolerance benefit from 7-12 %, with 2-3 % of that in silver for additional diversification. Younger investors with high risk tolerance can allocate 10-15 %, keeping the remainder in silver. Regardless of age, gold-related equities must be sold when in high demand and overpriced, because gold price is influenced by inflation rates and interest rates. Although gold is a safe-haven asset and a hedge against inflation and market volatility, its reliable record in times of market turmoil comes without yield, so the chosen allocation must balance protection with the need for annual income from the broader portfolio.

I created a baseline assignment of 5-10% of my yearly investiture asset to tangible precious metal and gold-backed assets. This spectrum constituted an important protection without endangering the prospect of my additional investments. A physical store of worth stayed steady when additional assets wavered, and it gave a psychological linchpin. In years of robust economic growth and steady markets I might rebalance toward the less point to take advantage of additional chances. The assignment is ever-altering and needs annual assessment.

Thomas GoldfreburgInvestor at Goldfreed

How does gold investment aid in diversification?

Gold's low correlation with stocks and bonds makes it an effective tool for portfolio diversification. By responding to economic conditions differently from traditional financial assets, gold lowers overall portfolio volatility, reduces drawdowns and mitigates tail risks. When equities, fixed income, or real estate fall sharply, gold cushions overall losses, helping investors preserve wealth. Its persistent negative-to-low correlation with US, UK and international markets allows a 2.5% weighting to lift Sharpe ratio by roughly 12%, illustrating boosted risk-adjusted returns.

Because gold moves independently of equities and credit cycles, advisors recommend it as a way to add diversification to a traditional portfolio of stocks and bonds while introducing an alternative asset. Gold is accessed via physical bars and coins, gold mutual and exchange-traded funds, or shares in gold mining companies, giving investors flexible routes to the same diversification benefits. For Japanese life insurers in particular, these diversification effects are the most compelling rationale for allocations, strengthening funding positions without increasing systemic risk.

The diversification advantage of precious metal constitutes a key depot of worth that extends beyond simple price action. By consciously initiating an asset category whose value trends are unaffiliated with the variations in conventional securities and debt instruments, I assign a part of my portfolio to precious metal. This non-correlation gives a steadying influence on my total asset wealth, because a part of my money is separated from the particular fates of any sole organization, business, or general sector. I regard gold as a type of financial protection against systemic dangers, for precious metal holds its worth and often acknowledges when other assets fall. Gold historically functioned as a secure harbor, and this helpful influence relieves the unpredictability that can damage long-term gain. I feel further assured in my fiscal plan of action.

Thomas GoldfreburgInvestor at Goldfreed

What is the best investment allocation comparison between equity, debt, and gold?

The best investment allocation comparison between equity, debt, and gold is given in the table below.

| Equity Allocation | Debt Allocation | Gold Allocation |

|---|---|---|

| 60%-65% | 25%-30% | Small portion |

| 50% | 40% | 10% |

| 60% | 30% | 10% |

| 40% | 50% | 10% |

| 70% | 25% | 5% |

| 80% | 10% | 10% |

| 90% | 0% | 10% |

| 50% | 30% | 20% |

| 86% | 4% | 10% |

| 20% | 65% | 15% |

| Equal weight (each) | Equal weight (each) | Equal weight (each) |

| 96% | 4% | 10% of equity allocation |

Between gold vs mutual funds, equity mutual funds earn higher long-term returns - typically 15-18 % over five years - while gold has lately delivered only ~10 %. Adding 10 % gold to a conventional 50-50 equity-debt portfolio improves the Sharpe ratio and reins in volatility to a 6-7 % band.

Aggressive investors can chase 12-13 % annualised returns with 90% equity, 0% debt, 10% gold or the slightly smoother 80 % equity, 10 % debt, 10 % gold. A balanced 60 % equity, 30 % debt, 10 % gold mix clocks 10-11 % returns yet keeps maximum drawdowns moderate. Equal-weight portfolios topped performance charts in five of the last seven calendar years, proving that gold need not be a mere satellite holding.

Over a 20-year SIP horizon, 50 % equity, 30 % debt, 20 % gold emerged as the most efficient choice: it delivered 10-11 % annualised growth, contained downside risk and offered the best trade-off between growth and safety. Retirees or stability-focused investors tilt to 40% equity, 50% debt, 10% gold, while those beginning long goals like children's education start at 70% equity, 25% debt, 5% gold and glide toward 50:40:10 by age 58.

Asset allocation is executed tactically through equity funds, debt funds and Gold ETFs. Periodic review and rebalancing keep the chosen mix intact.

Basic review resulting to acknowledge stabilizing part of different asset categories shows that allotment to precious metal demonstrated its value as non-correlated strength. My own way started with large dependence on assets. I observed bouts of exciting growth, yet assets confronted distress and much gain can disappear rapidly. Incorporation of liability given buffer during asset downswings and certain earnings flow steadied the structure.

Thomas GoldfreburgInvestor at Goldfreed

Expert behind this article

Thomas Goldfreburg

Thomas Goldfreburg is a gold investment advisor, author and founder of Goldfreed. Thomas's expertise is built on an academic foundation of a Bachelor of Science in Economics from Stanford University and complemented by market experience. Thomas specializes in gold IRA, ETF, 401k, and physical gold investments.