Gold has a well-burnished reputation as an inflation hedge, an attraction rooted in its long-standing function as a protector of wealth when consumer prices accelerate and currencies weaken. Because the metal tends to rise when the cost of living climbs, investors often treat it as a shield against the loss of real returns that accompanies monetary expansion and fiscal stress. Historical patterns show bullion frequently outperforms cash and many bonds during episodes of acute or unexpected inflation, a record that reinforces its value as a stabilising unit within a diversified portfolio.

Expert behind this article

Thomas Goldfreburg

Thomas Goldfreburg is a gold investment advisor, author and founder of Goldfreed. Thomas's expertise is built on an academic foundation of a Bachelor of Science in Economics from Stanford University and complemented by market experience. Thomas specializes in gold IRA, ETF, 401k, and physical gold investments.

Is gold a good investment during inflation?

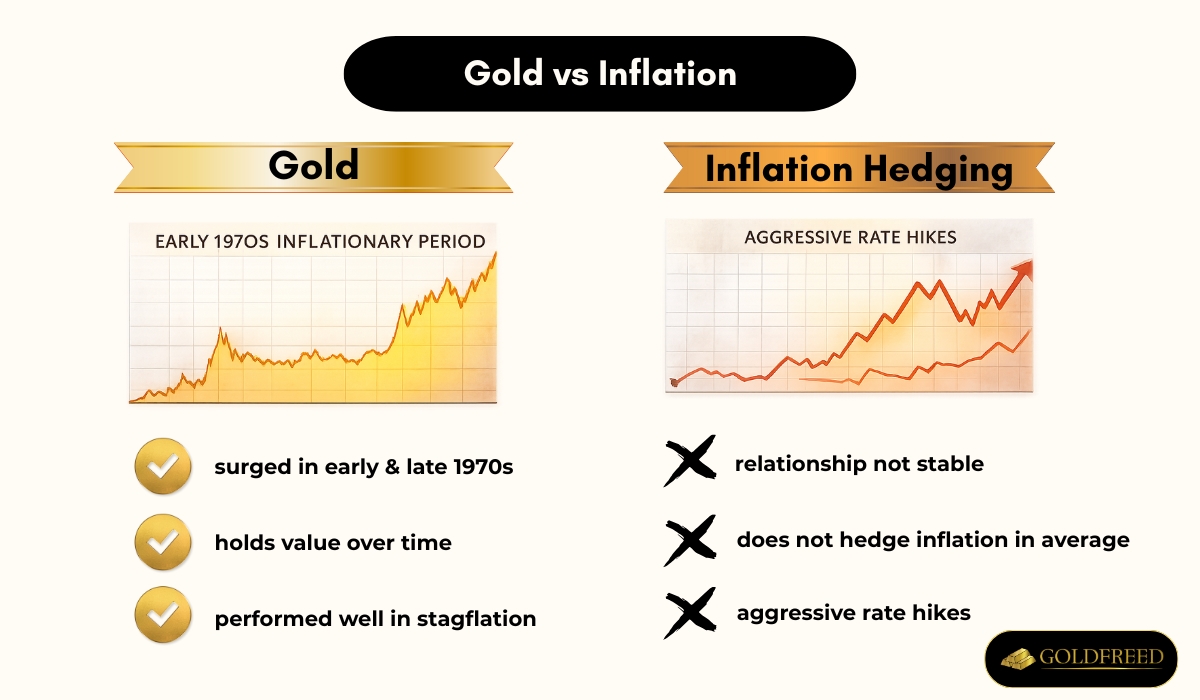

Private investors and central banks hold gold to store value, and gold has been hailed as a hedge against inflation because it often performs well while other investments struggle during economic downturns and inflationary periods. Gold excelled during the early and late 1970s inflationary periods, maintained its value when inflation surged, and performed well historically in stagflationary environments. Gold bullion has been one of the few asset classes to perform well historically in stagflation environments, and gold aficionados point to gold's ability to hold its value over time.

Yet the relationship is not stable, on average the answer is no, gold does not hedge inflation empirically speaking, and gold is not a blanket hedge against inflation. Gold is more a hedge against extreme unexpected inflation, and aggressive rate raising is not good for gold. Gold's part in a portfolio was not as an inflation hedge but as a store of value at a time of excessive and still growing government deficits. Gold is less likely to act as a hedge to equities but rather as a long-term store of value, and gold is not an effective way to protect equity gains in the short term.

My experience demonstrated that precious metal can act as a steadying influence during inflationary periods. The resource maintained my buying ability when the worth of paper money was decreasing, and the gold factor offered an offset. I chose to allocate a part of my reserves into tangible precious metal, and I regarded the ducats as a physical shop of worth. I saw the value of my precious metal holdings rise while my other assets experienced volatility or loss. This gave a feel of protection.

Thomas GoldfreburgInvestor at Goldfreed

How can using inflation data improve systematic gold and treasury investment strategies?

By using inflation trends to time the market, investors can enhance risk-adjusted returns compared with traditional buy-and-hold portfolios. Inflation data begins in 1913 and comes from the Bureau of Labor Statistics, episodes are identified retrospectively and subtract cumulative inflation from cumulative excess return on the asset, then cash is added to the asset return. TInflation event study has been extended to TIPS, broad commodities, and gold, confirming that inflation momentum inclusion improves the final model trading strategy.

Vanguard research shows that inflation beta-the predicted reaction of an asset to a unit of inflation-provides the most relevant measure of portfolio sensitivity for investors seeking to hedge inflation. Over the past three decades commodities had an inflation beta of about 6 to 10, while Treasury Inflation-Protected Securities provide one-for-one inflation protection because they are directly linked to the CPI. A goals-based inflation-beta-targeting methodology can therefore immunize a strategic portfolio with a specified inflation beta, and a time-varying portfolio construction approach adapts the optimal level of commodities to prevailing economic and inflation conditions. Gold's sensitivity is trumped by direct hedges: TIPS, yet gold still acts as insurance against the ongoing debasement of fiat currencies, especially when real yields are negative. Gold-backed exchange-traded funds, introduced in the early 2000s, allow rapid shifts between gold and other assets, broadening the investor base and making tactical implementation of the inflation-timing strategy both low-cost and liquid.