Gold has historically provided modest, appreciation-only returns: its annual average over various windows has run close to 10%, with the 20-year figure at 9.47%, while the three calendar-years ending 2023 saw a 2.9% pace. Because gold does not generate income through dividends or interest, every basis point of gain comes from price movement, making interest-rate shifts, dollar strength and investor risk appetite the principal drivers of performance.

Those same forces give gold a dual reputation. It is respected as an intrinsic store of value that has served savers for centuries, yet it is also one of the more volatile commodities, with annualised daily swings that regularly outpace broad equity indices. Over long horizons stocks have historically delivered larger cumulative rewards - the Dow Jones rose 991% during a period when gold advanced 360 percent - so gold's value proposition lies in timing and context rather than raw long-run return leadership.

Expert behind this article

Thomas Goldfreburg

Thomas Goldfreburg is a gold investment advisor, author and founder of Goldfreed. Thomas's expertise is built on an academic foundation of a Bachelor of Science in Economics from Stanford University and complemented by market experience. Thomas specializes in gold IRA, ETF, 401k, and physical gold investments.

What is the average return on gold investment?

The average annual return on gold has been approximately 8.69% since 1999, rising to 9.47% when measured over the twenty years that ended in 2024. Gold's annual average return was 13.8% in 2023 and over 28% in 2024. During the fifteen-year period that ended in 2023, the metal returned 5.8% annually on average. Bullion returned 16.94% on average during the seven crisis periods since 2007, evidence that gold performs better when real interest rates are low or negative and that a weakening U.S. dollar typically boosts gold prices. The average return on investment on precious metals, inclusive of gold, is around 3.5% annually when measured across the entire segment, while the average annualized return on gold itself is 6.8% if held for more than twenty years.

What is the history of gold investment returns?

Over two centuries, gold's purchasing power fell. A US dollar invested in gold in 1801 was worth just 78 cents by 1998, while the same dollar in stocks grew to more than half a million dollars and in bonds to nearly a thousand dollars. Between 1960 and the present the historical mean annual return is 8.4%, yet the ride has been volatile: the minimum annual return is -32.8% and the maximum is 120.6%. During the pandemic gold hit historic highs of $2,089 per ounce and surged to records again amid geopolitical tensions in 2024. Despite these bursts, global stocks returned 11.3% from January 1971 to December 2019, outpacing gold's sixfold increase over some windows. Gold's correlation to the S&P 500 is not stable. It has ranged from a coefficient of -1 to +1, and over long horizons the metal has exhibited a low, or sometimes negative correlation to equities and bonds, making it a crisis barometer rather than a growth engine.

What are gold investment returns in the last 10 years?

The gold investment returns in the last 10 years are given in the table below.

| Gold Investment Returns | Values |

|---|---|

| Last 10 years mean annual return | 8.8% |

| Stocks total return from 2004 through 2024 | 10.6% annualized |

| 2024 return | 27.20% |

| 2023 return | 13.14% |

| 2020 return | 25.75% |

| 2019 return | 18.28% |

| 2017 return | 9.54% |

| 2016 return | 8.62% |

| 2015 return | -11.61% |

| 2013 return | -27.61% |

| 2011 return | 7.80% |

| 2010 return | 30.60% |

| 2009 return | 25.04% |

| 2008 return | 3.97% |

| 2007 return | 31.59% |

| 2006 return | 23.92% |

| 2005 return | 17.77% |

| 2004 return | 4.40% |

Gold's last-10-year record is read in two complementary ways. Calculated as a compound annual growth rate, gold advanced 13.6% each year, turning every 1000 USD into roughly 1350 USD by the end of the period. Calculated as the simple mean of the ten yearly changes, the figure is 8.8%, a reminder that headline years like 2020 (+25.75%) and 2024 (+27.20%) sit beside quieter years like 2021 (-3.73%). In percentage terms the decade delivered a low-double-digit annual rate on average, materially above the 4% pace recorded during the 2010-2020 interval and close to the 10.2% mean of the last 25 years. Whether quoted as a CAGR or arithmetic mean, the 2015-2025 period ranks among gold's strongest modern-decade performances.

What are the monthly returns on gold investment?

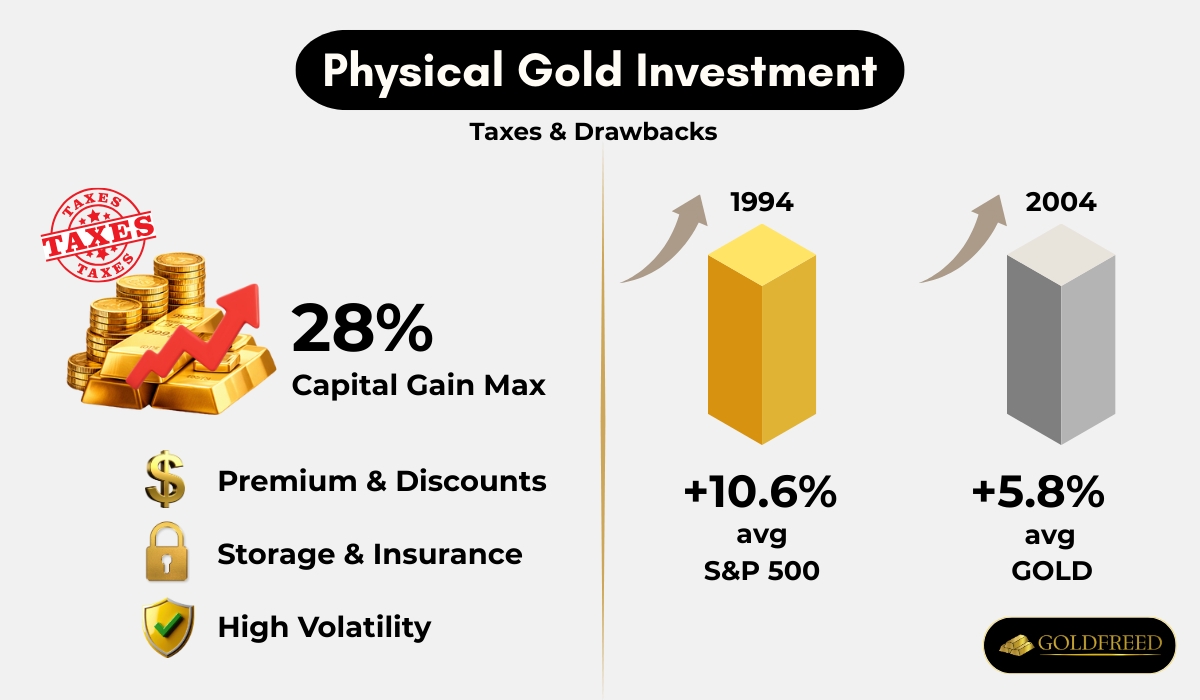

Every monthly investment becomes a precise weight of gold, with ups and downs during some months. Over short intervals the outcome swings sharply. Gold fell -7.27% in late 2025, illustrating that monthly performance is noisy. Gold ETFs are an important source of gold demand, but Gold ETF fees range from 0.15% to 0.40% each year, a drag that must be subtracted from nominal gains. Gold performs better when real interest rates are low or negative, a setting that often arrives when equities are weak. During such episodes gold is an inflation hedge when real interest rates are low and negative. While U.S. stocks beat gold over long periods - the S&P 500 generated an annualized total return of 10.6% before inflation from 1994 through 2024 and 7.8% after inflation - gold has low correlation with other major asset classes and surges when sentiment sours, as seen when the S&P 500 Total Return Index returned -7.24% on average during the seven crisis periods since 2007.

Therefore, a monthly saver expects scattered single-month losses alongside abrupt gains, while the multi-year stream of purchases smooths volatility and, under low-rate conditions, outruns both equities and inflation.

What are the returns on physical gold investment?

Physical gold is classified as a collectible by the IRS and is generally treated as a collectible, so gains face a top long term capital gains rate of 28%, a rate higher than on traditional assets. When acquiring coins or bars, buyers typically pay premiums above spot price, and when liquidating, they receive dealer discounts. Secure storage solutions and insurance costs are required, and these ongoing charges, together with the buy-sell spread, steadily erode returns. Gold price volatility, measured by annualised daily return volatility based on LBMA gold price, is considerable, and the metal performs less well when stocks are in a bull market. Over the three decades, ending in 2024, the S&P 500 generated an annualized total return of 10.6% before inflation, while gold, although serving as a hedge against inflation, delivered lower compounded gains. The net return to a private holder of bullion equals the change in spot price minus premiums, discounts, storage, insurance, and the 28% tax on any long term gain.

Tangible precious metal differs essentially from conventional financial investments, because its significance is in its function as a protector of principal rather than in creating profit. I do not assess its success in yearly or quarterly profits. Instead, I assess its capability to preserve buying power across years. The precious metal's return is yielded through principal appreciation over the protracted period, and its value frequently rises as trust in paper money declines. From my view, assessing precious metal's performance needs a varied mentality: I see tangible precious metal as a kind of financial protection and believe it to be a strategic possession for money security during times of economic uncertainty or heavy stagflation. Its past running history as a shop of worth is its significant return. It is a helpful influence on a portfolio, especially when additional investments decrease.

Thomas GoldfreburgInvestor at Goldfreed

What are the investment returns for gold and silver?

Gold reached $3,500 in April 2025, and gold trading reached $3,350-3,360 per ounce in July 2025. Gold and silver dominated year-to-date returns with the first half of 2025. Silver posted a 25.66% gain year-over-year, and its price is up about 80% year-to-date.

Gold and silver are significant in a diversified portfolio heading into 2026. Academic research suggests 5-15% allocation to gold or silver improves diversification. Silver provides higher growth potential driven by industrial demand and supply constraints. Silver is a higher beta metal than gold, meaning it is more volatile. Silver volatility averages 28.8%, and silver price swings are greater than gold. Silver is approximately 2-3 times more volatile than gold. Gold experiences less volatility compared to silver. Silver amplifies gains during commodity or industrial booms. Silver offers rising capital growth during economic storms. Silver offers higher growth potential driven by industrial demand and supply constraints.

Silver will play a strategic function in an investor's portfolio before 2026. Silver climbed to $38 in July 2025, and was estimated at $38.51 per ounce in the mid-2025 scenario. Silver provides industrial growth earnings, and more than half of all silver's demand comes from heavy industry and high technology. Silver growth is driven by solar panels and electric vehicles. Citi estimates silver price towards $40-$46, and expects silver to benefit from industrial usage. Silver outperforms gold when there is industrial growth and market optimization.

The S&P 500 generated an annualized total return of 10.6% before inflation from 1994 through 2024. Gold and silver are highly uncorrelated to the stock market and bond markets. Moderate Risk Investors target 3-5% silver, and aggressive investors target 3-6% silver.

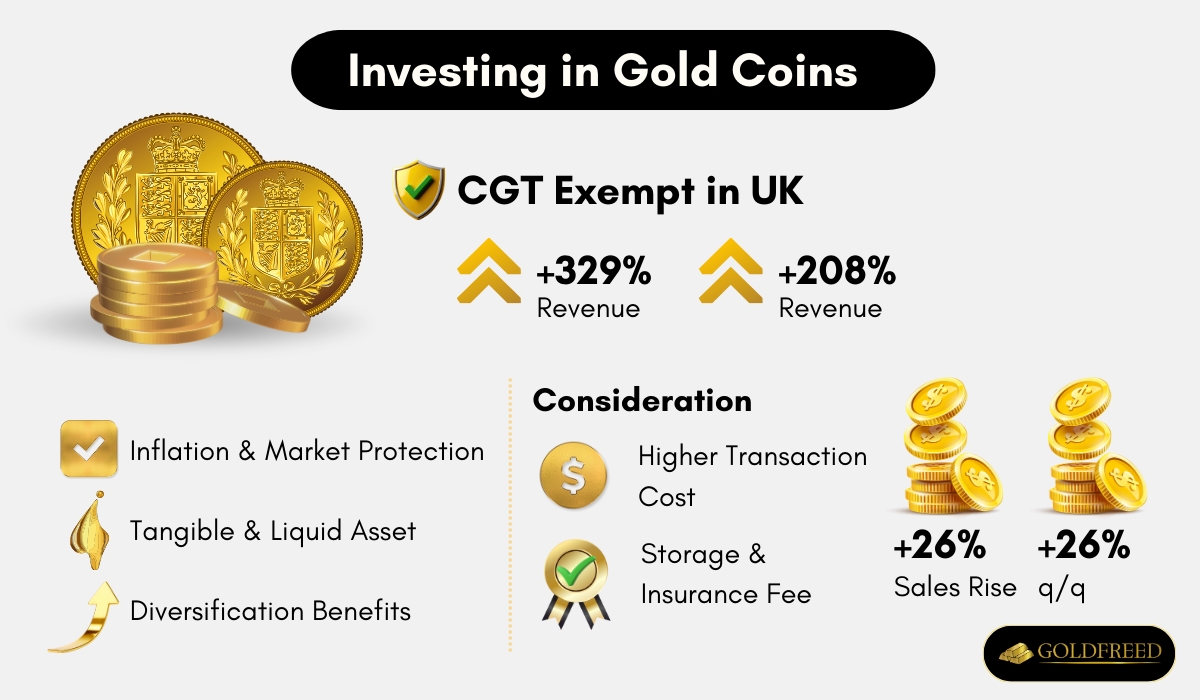

Are gold coins a good investment for returns?

Gold coins are a good investment, but returns depend on the specific coin and market timing. Gold coins are a relatively stable investment to preserve wealth and hedge against inflation, currency fluctuations, and market volatility. Gold coins are tangible assets and are highly liquid, allowing them to be sold worldwide. Gold coins derive their value and liquidity from the world market. Gold coins provide diversification benefits across various asset classes.

Gold coins have higher transaction costs than Good Delivery bullion, with round-trip dealing costs of 7 to 10 percent when bought through traditional coin dealers. Gold coins have additional costs of storage and insurance. Gold coins are neither the cheapest nor the safest way to buy gold. Good Delivery bullion is a cheaper alternative to gold coins, with a spread of 0.2% and maximum round-trip dealing costs of 1.2%. Good Delivery bullion commission at purchase is 0.5% and commission at sale is 0.5%. Gold coins have risk of fakes and forgeries and are subject to fraud if a dealer does not pay or deliver within 30 days. Gold coins have a poor resale price when you want to sell.

Gold coins are exempt from capital gains tax (CGT). Royal Mint data shows gold coin revenue increased 329% and total weight of gold coins sold rose 208% year-over-year. Gold coin sales rose 26% quarter-over-quarter. Gold bullion coins are issued by the Royal Mint and are exempt from capital gains tax. Gold coins are stored in a financial institution's vault or safety deposit box, but storing and insuring them is expensive. Gold coins are insured, but storage at home carries a risk of theft. Many users began by looking at how they must buy gold coins and then altered their mind and bought Good Delivery bullion instead.

I found that precious metal coins are not a passive investment, the deal expenses involve merchant fees and charges over the spot cost, while safe keeping and coverage comprise ongoing costs that must be added into the overall figure of profits gain. The tangible quality of the metal supplied a feel of safety that paper investments could not duplicate, yet the returns were volatile like some assets and the deal prices could decay . I saw their cost appreciate steadily especially during times of economic uncertainty, so I bought one-ounce coins from a respected vendor and found that the biggest advantage materializes when keeping the metal money for a substantial period, making me see them as a long-term shop of worth.

Thomas GoldfreburgInvestor at Goldfreed

Is gold investment and returns worth it?

Gold investments will be worthwhile in 2025. Investors add gold to diversify portfolios because gold has low correlation with other major asset classes. Gold price is uncorrelated to stocks and negatively correlated to the stock markets. When other markets fall, gold often rises, so gold comes out the winner during market downturns. Banks buy gold to hedge against inflation, and gold ETFs are popular with institutional investors for the same reason.

Gold is perceived as a safe-haven asset that will retain its value, and gold shines brightest during geopolitical uncertainty. Because gold is a precious metal with fewer industrial uses, it is less affected by economic declines. Thus gold provides a hedge in a potential economic or market downturn. Gold investment companies let you borrow against gold bullion, adding liquidity to the position.

Forecasts indicate solid returns: gold will reach $4,500 per ounce later in 2025, while a more conservative gold forecast projects $3,700 per ounce by the end of 2025 and gold price will hit $4,000/oz by mid-2026.

Gold's value is in its function as a trustworthy store of worth, not simply in its price appreciation. I began with tiny acquisitions of coins and an ETF backed by tangible gold, propelled by a yearning for stability. One should not anticipate performance equal to high-growth securities as its yields are modest. The real prize occurs during economic uncertainty or heavy stagflation. When additional investments stumbled I saw substantial volatility in ordinary shares. I remember a particular episode when geopolitical hostilities prompted market fear, my precious metal holdings stayed stable and worked as a financial mainstay, giving a deep sense of safety while lessening overall portfolio volatility.

Thomas GoldfreburgInvestor at Goldfreed