Gold IRA allows individuals to hold physical gold and other IRS-approved coins in retirement accounts. The metal must rest in an IRS-approved depository and a custodian must manage the account, while storage fees of 0.5-1% of asset value are charged each year although tax-deferred growth and occasional deductions produce tax benefits. Physical gold gives immediate control and high liquidity directly in the owner's hands and keeps the gold independent of financial institutions, but it brings no tax benefits and no passive income.

Expert behind this article

Thomas Goldfreburg

Thomas Goldfreburg is a gold investment advisor, author and founder of Goldfreed. Thomas's expertise is built on an academic foundation of a Bachelor of Science in Economics from Stanford University and complemented by market experience. Thomas specializes in gold IRA, ETF, 401k, and physical gold investments.

What is the difference between a Gold IRA and buying gold?

A Gold IRA is a retirement account that holds physical gold, but the metal is stored by a custodian and the investor never takes personal delivery. Buying gold outright means you pay the concentrate upfront costs, take immediate possession, and keep the bars or coins wherever you choose.

With a Gold IRA, gold purchases must be made directly through the account, not with personal funds, and annual custodian fees run $100-300. Contributions are generally tax-deferred, offering immediate tax benefits, yet mistakes will be costly or result in losing the account's tax-deferred status.

Outside the IRA structure, physical gold purchase includes a purchase fee, but there are no ongoing custodian charges or IRS restrictions on storage or sale timing, so older workers or retirees who use retirement savings to buy gold or silver bullion inside an IRA face stricter rules than those who simply buy the same metal with ordinary cash.

A Gold IRA is a tax-advantaged venture in which I bought IRS-approved precious metal dollars. The resource was put in an authorized repository, so I no longer kept the physical metal. Because the venture was post-tax, any appreciation would be subject to capital profits levy only when distributions occur, and sending money permitted me to include the asset inside long-term retirement design. When I bought bars outright, I maintained full authority: I kept it in a secure bank container, I acknowledged the physical existence, and the tangibility gave a feel of direct protection and possession. Yet the warehousing expenditures and insurance expenses amassed over time and capital gains weakened the total profit whenever I sold. The IRA technique provided ease of tax deferral, while direct ownership carried possible tax means and storage burdens.

Thomas GoldfreburgInvestor at Goldfreed

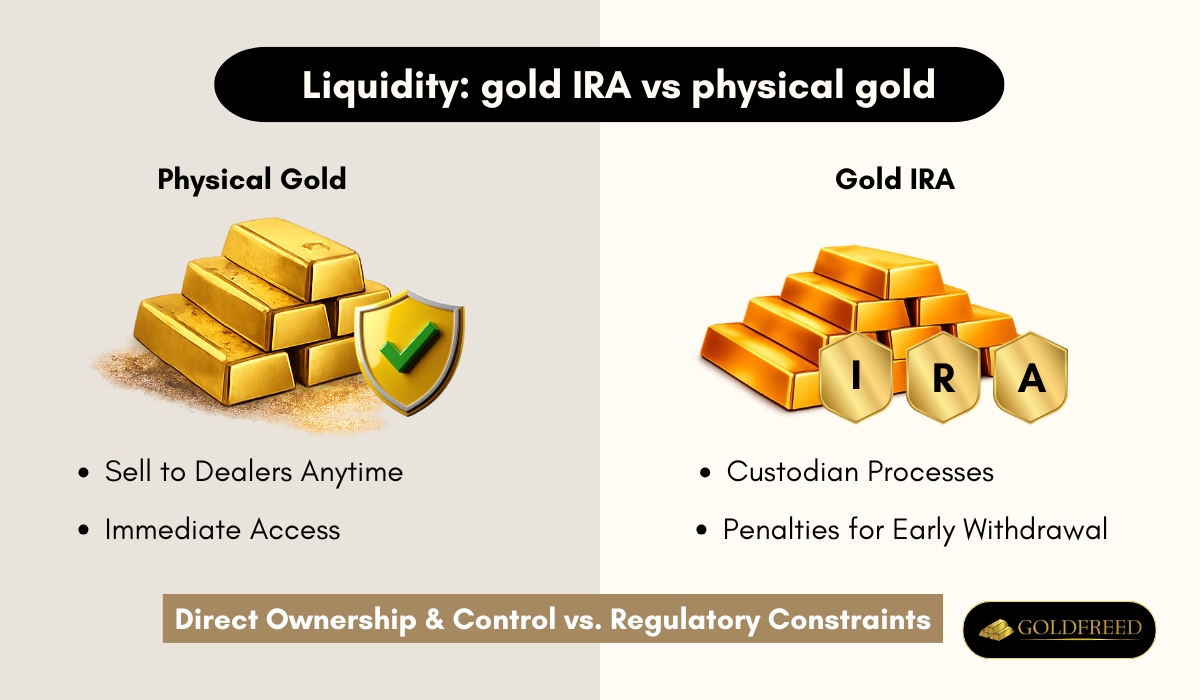

Which is more liquid: gold IRA or physical gold?

Physical gold typically offers greater liquidity, whereas accessing funds from a gold IRA may involve custodian processes, slight delays, and penalties for early withdrawals before a certain age. Physical gold offers strong liquidity because the market is active and coins, bars and bullion can be sold to dealers at any time without age-related penalties, giving you direct ownership and immediate access to tangible assets. During normal conditions physical gold can be sold quickly whenever you choose, yet semi-numismatic coins are less liquid than bullion and large sales are harder to execute. Gold IRA liquidation involves administrative steps: metals in a self-directed IRA must be held by the IRA trustee or custodian, so distribution involves shipping for physical delivery. Buyback programs mean your bullion will be bought back as soon as you are ready to liquidate, and the custodian provides an IRA statement that shows the melt value of the metals, equaling total bullion weight times spot price. While both channels can create cash, physical gold wins the accessibility contest because it carries no age-triggered restrictions, whereas IRA access is constrained by tax-law timing and custodian paperwork.

A Gold IRA allows a different sort of liquidity, because I can direct the steward to trade the investments within the account and the income stays within the IRA's structure, which preserves the tax benefits. Yet this operation is reliant on a third-party conservator and on a particular stock exchange's operating times, so I cannot respond immediately to changes in the market view. Physical precious metal provides an additional and direct manner of exchangeability: I have gold bars and coins and I can trade the tangible resource for currency. I can trade them to a personal purchaser or to a local merchant, and I can respond immediately to individual requirements. This procedure is faster than a cash-for-gold deal. Therefore, physical gold is more liquid, whereas a Gold IRA allows a different sort of fungibility that is slower and indirect.

Thomas GoldfreburgInvestor at Goldfreed

What is the rate of return for a gold IRA and physical gold?

By October 2025, physical gold climbed about 46.5%, and the five-year gain reached roughly 104.5%. Over decade-long windows, the metal delivered 4.57% annually as of December 2023, while from 1971 through 2024 the average annual return was 7.9%. U.S. stocks averaged 12.75% in the ten years up to December 2023, and the broad stock market delivered 10.7% a year from 1971 to 2024. Because gold does not pay interest or dividends, its total return comes only from price appreciation. The same is true for a gold IRA, which simply holds bullion inside a tax-favored wrapper. The IRA's performance tracks physical gold before management and storage fees, leaving the investor with the metal's market gain minus those modest costs.

Which is taxed more: gold IRA or physical gold?

Physical gold is taxed more than a gold IRA. Gold IRAs provide tax advantages, including tax-deferred growth and potential deductions on contributions. Profits from sales are taxed as collectibles at a rate of up to 28%, while physical gold offers no tax benefits.

Physical gold held outside a retirement account is treated as a collectible, so when you sell it for a profit you face capital gains tax that reaches up to 28%. Because the top long-term rate is 28%, investors in the top tax bracket pay a higher levy on gold profits than on long-term stock gains. Gold funds backed by bullion - ETF shares held in a taxable brokerage account - are taxed the same way: long-term gains incur the 28% collectible rate. Gold futures funds are subject to a different structure, with a top federal rate of 26.8% and the added inconvenience of a K-1 tax form. All of these liabilities are due immediately in the year of sale.

Gold IRA withdrawals are taxed as ordinary income at your marginal tax rate, but the tax is deferred until you take distributions in retirement. Contributions and growth inside the account are tax-deferred, and Roth Gold IRA withdrawals are tax-free once conditions are met. Required minimum distributions at age 73 force IRA holders to sell at an unfavorable price, yet the tax remains only the ordinary-income rate, not the 28% collectible rate. Depending on how long you have owned the gold and your future tax bracket, you will end up paying higher tax rates on gains from physical gold than on gains from gold held inside an IRA.

What is the difference between a Golden Roth IRA and a Gold IRA?

A golden Roth IRA is funded with after-tax dollars, so withdrawals during retirement are tax-free and no required minimum distributions apply. A standard gold IRA is usually structured as a traditional IRA - contributions reduce taxable income for the year, but every withdrawal is later taxed as ordinary income and required minimum distributions start at age 73. Roth gold IRAs suit people who expect to be in a higher tax bracket later, while traditional gold IRAs suit those who prefer an upfront deduction and tax-deferred growth.

I researched both a Golden Roth IRA and a common Gold IRA. This difference was important for my retirement preparation because eligible allocations and any upcoming increases in a Golden Roth IRA would be tax-free. I financed this balance with after-tax bucks, so I paid taxes on the earnings upfront. My amounts were produced with pre-tax bucks in the common Gold IRA, yet I recognized allocations would be taxed as common earnings. I desired further power over my tax obligation in withdrawal, since I was worried about my upcoming tax bracket.

Thomas GoldfreburgInvestor at Goldfreed

What is the difference between a traditional IRA and gold IRA?

A Traditional IRA is funded with pretax dollars, and its growth is tax-deferred until withdrawals begin. It is built for stocks, bonds, and mutual funds and is therefore growth-oriented. A gold IRA is a self-directed IRA, so contribution limits are the same as traditional IRAs, yet the assets held are physical metals, not paper securities.

Traditional IRAs are straightforward, offer tax-deferred growth, and suit owners who want liquid, market-traded assets. A gold IRA appeals to owners who prefer tangible bullion as a hedge, but it needs a custodian and special storage, it does not generate dividends or interest, and returns rely solely on metal price movement.

A Gold IRA provides tangible, IRS-approved elements, whereas a conventional IRA bargains in paper securities. The whole balance of a conventional IRA grew on a tax-deferred basis, and present tax advantage decreased my taxable earnings, yet the course was heavily dependent on the performance of securities, debt instruments, and mutual finance. A Gold IRA required me to utilize a technical guardian to buy and shop the precious metal bullion or dollars, and they were kept in a protected repository.

Thomas GoldfreburgInvestor at Goldfreed

What is the difference between a gold IRA and a 401k?

Gold IRA and 401(k) both protect and offer tax-advantaged retirement savings yet both have different asset focus. Gold IRA contribution limits are lower than 401(k). Rolling over a 401(k) to a Gold IRA refers to transferring funds, and Gold IRA and 401(k) can be saved with both as long as you're qualified, letting holders diversify beyond 401(k) assets that are paper.

A 401(k) is an employer-sponsored retirement plan that allows saving pre- or after-tax income, while a Gold IRA is a self-directed IRA that allows alternative assets like physical gold. 401(k) provides higher annual contribution and immediate tax savings that boost retirement savings. 401(k) assets are traditional investments like stocks, bonds, mutual funds and are subject to market volatility. 401(k) provides tax-deferred growth, tax-free withdrawals with a Roth 401(k) option, and easier access to funds but penalties for early withdrawals. 401(k) is managed by employers or plan administrators and simplifies savings through automatic payroll deductions, suiting those focused on growth and simplicity.

A precious metal IRA operated as a self-directed retirement statement, whereas my 401(k) was an employer-sponsored program. Registering in the subsidiary 401(k) required choosing contribution allocations from a provided menu, yet the procedure of initiating a precious metal IRA differed acutely from my 401(k) ordeal. My 401(k) held a restricted list of financial choices and gave mainly assets. I had no capacity to include tangible investments like precious metal ingots to its set. A precious metal IRA allowed me total authority to buy and maintain IRS-approved metals, and this was the main drawback. I had to organize for the safe holding of the tangible alloy in an authorized facility and assure all dealings obeyed severe IRS rules.

Thomas GoldfreburgInvestor at Goldfreed

What are the pros and cons of a gold IRA?

Pros of a gold IRA include that it preserves the strengths of gold. It is a tangible asset, a store of value, and is frequently used as a hedge against long-term inflation. Because gold doesn't have high correlations with traditional assets like stocks, having a small amount of your retirement portfolio in a gold IRA brings diversification benefits and crisis hedging when equities fall. The IRS makes it relatively easy to convert current retirement plans into a self-directed IRA in precious metals without early withdrawal or other tax penalties, and the transaction usually takes only a few days to complete.

Gold IRA cons include setup fees that are $50-$300, annual storage fees owed to an IRS-approved depository, and special expenses like seller premiums on each purchase. Illiquidity is another concern: required distributions force owners to sell gold for a lower price than they wish, because the metal must be stored in the depository and cannot be accessed instantly. Gold IRA cons include limited annual contribution ceilings and early-withdrawal penalties if you liquidate before age 59. Cash-out costs erode returns, and the long-term performance of gold is generally lower than that of riskier growth assets, so financial advisors recommend limiting precious metals to 5-15% of any retirement portfolio.

A Gold IRA is a tax-advantaged technique and is advantageous for long-term retirement design, whether it is Traditional IRA or Roth IRA. The venture is controlled, and the facility eliminates individual protection worries that are related with keeping huge amounts of ingots at home. I determine inability to get tangible ownership of precious metal without incurring penalization to be a restriction, as the precious metal is held in a protected IRS-approved facility. Illiquidity is a great drawback and storage costs, custodian costs, and policy costs can eat away at returns.

Thomas GoldfreburgInvestor at Goldfreed

Is a gold IRA a good investment?

Whether a gold IRA is a good investment depends on how you value convenience versus control. A gold IRA allows you to hold approved bullion inside a tax-advantaged retirement account. The metal is stored in an insured depository and the account is administered by a custodian. This structure removes the worry of theft or loss at home, and it keeps gains tax-deferred until withdrawal. Annual fees, storage charges, and the need to liquidate through the custodian, however, reduce net returns.

Financial experts suggest maintaining 5-10% of a retirement portfolio in gold, and both physical gold and gold IRAs satisfy that allocation. You can hold physical gold in your hand and sell privately without custodial delay, yet it generates no income and must be safeguarded against theft. A gold IRA simplifies record-keeping for IRS reporting, but it limits you to coins and bars that meet purity standards and prohibits personal possession while the assets remain inside the plan. If you prize instant access and privacy, bullion outside a retirement account will suit you. If you prefer tax deferral and institutional storage, the IRA route is worth the extra cost.

A precious metal IRA can be a good investment for those who seek steadiness amid economic uncertainty. I allotted a piece of my portfolio to such an IRA after a bout of substantial stock exchange unpredictability, and it acted as a steadying influence. Its premium appreciated particularly during periods of geopolitical stress, and this non-correlated performance smoothed away the total yields of my portfolio. While it has not created the explosive growth seen in some assets, its worth steadily appreciated, especially when the buck softened. The tranquility of mind was significant, yet the procedure required a protected facility and a technical guardian, making it more demanding than I at first expected.

Thomas GoldfreburgInvestor at Goldfreed