The answer to whether gold is a tax-free investment depends on where and how you hold it. In some jurisdictions, investment gold is exempt from Value-Added Tax, yet in India it is taxed at 3 %. Inside a self-directed IRA or 401(k), the appreciation is not subject to capital gains taxes as long as the metal stays within the account, making retirement wrappers a strategic tool. Outside such wrappers, the Internal Revenue Service stands out: it deems physical gold a collectible, so federal capital-gains rates can reach 28%, higher than the rates on most other investments. Losses on gold and silver can be used to offset other capital gains, and a physical-gold CEF is taxed at favorable long-term capital-gain rates.

Is gold a tax free investment?

No wholesale blanket exemption exists, but several narrow, well-defined situations allow gold to move through the ownership cycle without immediate taxation. Long-term capital gains on stock and bond sales face a maximum 20% tax rate, whereas gold is an investment asset, so when you sell your gold and make a profit, it is taxed as capital gains.

First, the form matters. Investment-grade bars and coins that meet national bullion purity standards are usually free of sales tax or VAT at the moment of purchase. For example, Canada omits GST/HST on qualifying bullion, Australia exempts investment gold from GST, and the European Union waives VAT on bars and coins formally classed as investment gold under interim regulations. Second, geography matters. Residents of Maine, Virginia, and New York can buy or sell precious metals without state-level sales or use tax, although federal capital-gains rules still apply when the metal leaves their hands. Third, timing matters. In most jurisdictions, including the United States, profit realized after the metal has been held for more than twelve months is classified as a long-term capital gain. Long-term gains enjoy a reduced top federal rate of 20% instead of ordinary-income brackets, but the tax agency simultaneously classifies physical gold as a collectible, so the special ceiling rate of 28% applies, meaning the entire profit is taxable even though it is deferred until sale. Retirement wrappers create a further layer of relief. Gold held inside a traditional IRA grows tax-deferred, while qualified withdrawals from a Roth Gold IRA are completely tax-free once the account has been open at least five years and the owner is older than 59. Traditional Gold IRA withdrawals are taxed as ordinary income.

These concessions do not convert gold into a universally tax-free asset. Short-term holdings - twelve months or less - generate ordinary-income treatment, and if annual exemption thresholds are exceeded in the EU, the entire gain becomes taxable. Losses from gold or silver positions are used to offset other capital gains, but they must be reported. Because residence, form, holding period, and vehicle choice each change the outcome, potential investors must consult a qualified tax expert before relying on any of these limited exemptions.

I retain the belief that precious metal is not a tax-free venture. The concept that gold exists in a particular tax-exempt class is a risky misconception. Income I earn from trading a metal bar or coin is subject to capital profits tax. An increase in the price of precious metal is categorized as an asset benefit, I must declare these taxes. Although buying tangible precious metal may not incur a prompt levy, a tax obligation is initiated when I sell at a gain. This element diminishes the total return on a venture in precious metal.

Thomas GoldfreburgInvestor at Goldfreed

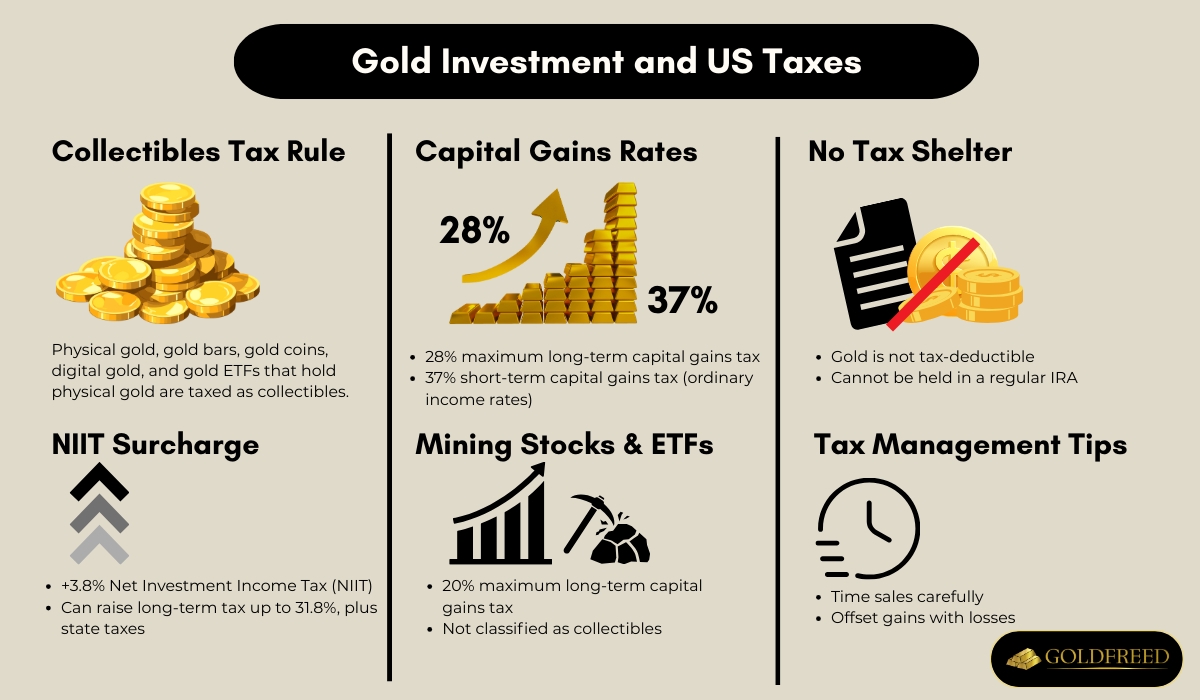

What is the tax rate on gold investment?

Physical gold, gold bars, gold coins and similar bullion are classified by the IRS as collectibles. Long-term capital gains on these assets are therefore taxed at a maximum rate of 28 percent, a rate that also applies to shares of exchange-traded funds and mutual funds that hold physical gold because such funds are structured as trusts holding the metal itself. The same 28 percent ceiling governs digital gold held longer than twenty-four months, since tax law treats it as the economic equivalent of holding bullion. Gains from any of these forms of gold held one year or less are short-term and taxed at ordinary federal income rates up to 37 percent, while an extra 3.8 percent net investment income tax applies to either short- or long-term gains if the investor's income exceeds the statutory threshold, producing a blended top federal rate as high as 31.8 percent on long-term positions.

Investors who want equity exposure rather than the metal itself can buy gold-mining stocks or ETFs that hold such shares. These securities are not collectibles, so long-term gains are capped at the standard 20 percent federal rate and short-term gains are again taxed at ordinary rates. Once the federal liability is computed, most states add their own income tax on the gain, further raising the after-tax cost of selling.

No feature of the U.S. Internal Revenue Code makes gold investment tax-deductible, nor does the law allow the metal to be held inside a regular IRA. Only a self-directed IRA that meets strict custody and purity rules can own physical gold, and even the distributions are eventually taxed at ordinary rates. While investors sometimes view gold as a hedge, it offers no special shelter from current taxation. The only way to avoid tax is to time realization of gains, harvest losses from other investments, or hold the position until death so heirs receive a stepped-up basis. Gold is not tax-free: physical forms face the 28 percent collectibles rate, mining equities face the 20 percent standard long-term rate, and every sale carries an extra 3.8 percent NIIT plus state tax, making careful timing and record-keeping vital to managing the final bill.

Expert behind this article

Thomas Goldfreburg

Thomas Goldfreburg is a gold investment advisor, author and founder of Goldfreed. Thomas's expertise is built on an academic foundation of a Bachelor of Science in Economics from Stanford University and complemented by market experience. Thomas specializes in gold IRA, ETF, 401k, and physical gold investments.