Gold and the U.S. dollar rarely march in step. Because bullion is priced in dollars, a weaker dollar automatically lowers the metal's market price for foreign buyers, while a firmer unit raises it; thus, historically, the two values have moved in opposite directions. Different risk-off episodes illustrate the pattern: when fear sweeps markets, capital flees toward one safe haven and away from the other, so gold price rises while the dollar depreciates, or the reverse. Traders treat both instruments as flight-to-quality assets, yet their incentives diverge. A strengthening dollar makes gold less attractive because the metal yields nothing, whereas cash can earn interest; conversely, rising inflation or geopolitical stress sends investors to the non-yielding asset that provides a hedge against market volatility and purchasing-power loss. Observing this persistent inverse link, central banks have steadily diversified away from dollar reserves, purchasing record amounts of gold even as they acknowledge that each asset waxes and wanes with the cycle of growth, rates, and sentiment.

Is gold a better investment vs the US dollar?

When U.S. interest rates rise, gold becomes less attractive, yet the very same move later weakens the dollar and thus makes gold cheaper for holders of other currencies. On calm days cash earns a yield and circulates easily, on volatile days the metal's absence of counter-party risk outshines the currency's convenience.

Established wisdom endorsed the US dollar as the safe-haven resource, so I allocated a considerable part of my funds into high-yield savings and believed in the steadiness of the money. Inflation arose intensely, and the actual price of my dollar-denominated properties was decreasing attributable to rising prices, my dollar investments stagnated. I noticed a continual decline in my purchasing capability, and this made me branch out into tangible gold. Gold has an inherent amount that has persisted for centuries. My initial gold coins gave physical protection, while my digital cash holdings could never offer physical protection. The value of my gold holdings increased, confirming that gold can outperform when the US dollar weakens.

Thomas GoldfreburgInvestor at Goldfreed

Which performs better in the long term: gold vs US dollar?

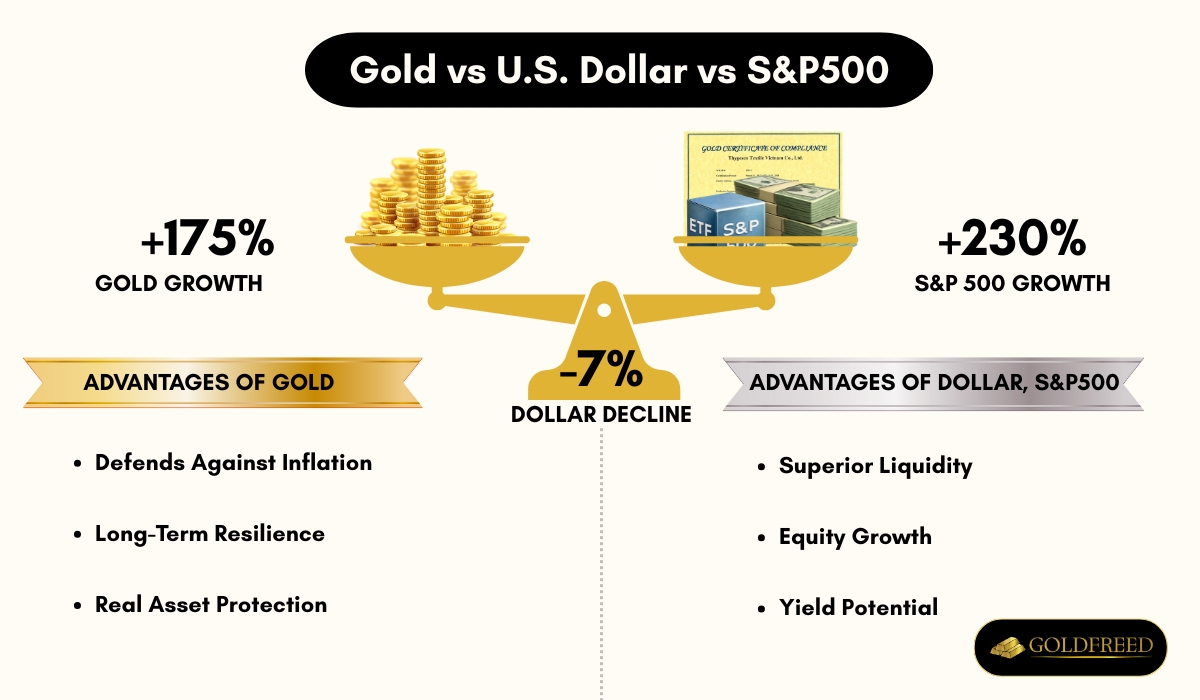

Since 2008 gold has outperformed the U.S. dollar, the S&P 500 and most other reserve-currency assets. Over the same horizon the U.S. dollar index, which measures the dollar against a basket of currencies, has fallen 7%, while gold is up 31% in 2024 alone and roughly 7% since late September even as the index itself rose nearly 10%. Gold's advance has occurred while long-term U.S. rates climbed by almost a full percentage point, showing that the metal strengthens when the dollar looks strong in nominal terms.

The long-term secular drivers remain firmly in place: unsustainable U.S. budget deficits, central-bank diversification into gold, and the reordering of the global trading system under a slow de-dollarization theme. These macro drivers create an asymmetric payoff: gold moves first as it reacts to fiat-currency debasement, whereas the dollar's upside is capped by the same fiscal imbalances that ultimately support gold.

Gold is volatile in the short term - its price swings sharply with real-return surprises - yet it acts as a store of value when U.S. exceptionalism is questioned. Because it is a non-yielding asset, gold performs better when real interest rates are low or negative, higher real yields decrease gold price, while falling real yields increase it. Thus, over thirty-year windows gold has outperformed bonds and, in several periods, the S&P 500, delivering a hedge against both currency depreciation and equity drawdowns while the dollar offers relative safety against other fiat units.

Gold mostly plays better as a long-term protection against systemic risks and monetary reduction. My experience has shown gold possesses long-term resilience. I see gold as a foundational asset for maintaining principal across years, for inherent value exceeds public boundaries. During times of monetary tightening, the US dollar strengthened, yet its value remains susceptible to the state of the American economy and the policies of the Federal Reserve. There have been durations of intense economic growth, but I recall times of substantial inflation when the purchasing power reduced and trust in cash wavered. Consequently, gold performs as a dependable store of value, while the US dollar offers uncomparable liquidity for transactions, yet cannot match gold's steady protection over decades.

Thomas GoldfreburgInvestor at Goldfreed

Is gold a safer investment than US dollar?

Gold is a classic safe-haven asset that investors embrace when they fear losing real value from cash or U.S. government bonds. Conventional investing wisdom therefore treats gold as the default shelter during a global crisis, yet the metal is not a uniformly safe investment.

Price charts show gold works as a haven in lower-interest-rate conditions, because lower interest rates reduce the yield opportunity-cost of holding bullion, but outside such periods gold often trades more like a risk asset, and its daily price swings rival equities. Several analysts conclude that gold is a safer choice for long-term investing, but only so long as geopolitical risk dominates the narrative. When the dominant fear is enterprise-level or systemic financial leverage, gold trades like risk assets and the price drops alongside stock indexes.

U.S. Treasuries are an alternative to holding gold when the goal is pure stability. Treasuries are seen as safe assets backed by the taxing power of the United States, and they do not collapse on days equity markets fall. Gold cannot be printed by central banks, which explains why countries buying more gold use it to diversify reserves away from the dollar-based banking system. The result is a slow but steady shift: gold has transitioned from a cyclical safe haven to a structural necessity. Reserve managers have realized they will buy gold simply to escape potential sanctions or currency freezes, rather than to chase short-term profits.

Explaining the entirety of the gold-versus-dollar safety question therefore requires two simultaneous lenses. First, gold delivers protection against acute currency debasement and heightened global tensions. Second, within normal business cycles, gold's volatility and the tendency of central banks to manage liquidity through U.S. Treasury issuance reduce its day-to-day risk superiority. Thus gold is typically a safer choice only when tail risks define the market mood. Investors who construct portfolios under the assumption of unending peace, low inflation, and rising real rates discover that the frequently quoted mantra, gold is a classic safe-haven asset, applies more to the survival kit than to the trading ledger.

Gold has historically acted as a trustworthy shop of value during times of uncertainty, while the dollar gives direct buying capability and stability within the system I work in. I recognize that gold is not exposed to inflation as fiat money, yet the dollar is unequaled in its use and approval. The supply of gold is limited, and this underlying rarity gives me a feel of safety, my money is fixed to a physical asset with intrinsic value. A government can depreciate its monetary system, whereas my gold assets are not dependent on the monetary policy of my country. Gold's price can be unstable in the short term, so I also recognize the US dollar provides a contrasting kind of security.

Thomas GoldfreburgInvestor at Goldfreed

Which is a better hedge against inflation: investing in gold vs dollar?

Gold is often hailed as one of the most prominent inflation hedges, its reputation burnished by decades in which its price rises whenever inflation rises. Investors rush to gold when they see currencies losing value, and the 1970s oil shocks offer the textbook case: inflation soaring caused gold to jump from $35/oz to $800/oz. Yet that episode also hints at limits, for gold slumped after dollar strength and the 10-year Treasury yield dropping below 4%, showing that the metal falls even while consumer prices remain raised.

Over long horizons the picture shifts further. Sinead Colton Grant notes that equities, not gold, are a much better inflation hedge over the long term, and BNY echoes that US stocks are the smarter inflation hedge. Gold's function in a portfolio, therefore, is less as an inflation hedge than as a store of value that calms a portfolio when a shock hits, combining gold with other inflation hedges, for example, real estate, TIPS, and select stocks creates a more resilient portfolio.

Commodities add another layer of protection. Commodities look like the better bet as opposed to gold for investors specifically seeking a hedge against inflation risk, and silver and gold themselves do a really good job of hedging inflation when there's a shock. Treasury Inflation-Protected Securities provide built-in inflation protection, while government bonds have shown to pay higher rates when inflation rises. Thus the dollar, whose value erodes as inflation causes currencies to lose value over time, is best used through instruments that automatically adjust coupons or rents rather than through idle cash.

I do not regard the U.S. dollar a sure hedge, for inflation debases the U.S. dollar and retaining dollars during inflation results in a decline of real value. Gold has historically kept its buying power, because central banks cannot produce gold at will and its rarity is its strongest point. The function of a hedge is to keep purchasing ability, not simply to outperform another fiat money, gold's price is absolute, while dollar's power is relative to different currencies.

Thomas GoldfreburgInvestor at Goldfreed

Which offers better returns: gold vs dollar investment?

Gold has historically provided consistent returns. From January 1971 to December 2019 gold had average annual returns of 10.6%, while the dollar had annualized returns of 18.49% across overlapping samples. Dollar annualized returns 18.49%, yet gold had annualized returns of 30.16% over that period, and gold had annualized returns of 17.79% during separate intervals. Gold returns depend on the period under consideration, during crisis scenarios gold had annualized returns of 7.16%, while Treasurys had annualized returns of -2.74%, and gold appreciated ~8% on an annual basis over the past 20 years.

Higher interest rates attract money away from gold into higher-yielding investments because gold is a non-yielding asset and real yields present the opportunity cost of holding gold. Higher interest rates make gold less attractive, nevertheless gold is up roughly 7% despite U.S. interest rates spiking higher, the dollar demonstrated major strength simultaneously, and gold price is influenced by real interest rates. Lower returns from cash investments prompt retail investors to rebalance their portfolios in favor of gold, gold is up 3% year-to-date beating stocks, gold price is up 31%, and gold price is influenced by systemic risks.

Gold provided no return beyond nominal increases, yet the nominal increases were reassuring when the dollar assets gave steady benefits. I allocated a considerable part of my reserves into dollar investments, and this strategy offered certain returns, but it produced small proceeds. My gold assets rose significantly, while the buying strength of my dollar wealth weakened during times of heavy inflation, as the actual worth of the dollar was reduced even though the nominal face value rose. Gold involved holding costs, yet I recognized the reduced risk it offered when its price showed a strong opposite direction with the dollar's movement.

Thomas GoldfreburgInvestor at Goldfreed

What are the pros and cons of investing in gold vs dollar?

Gold investing cons include it doesn't produce income, it does not generate dividends or any passive cash flow, and physical holdings incur storage and insurance fees plus capital-gains tax when sold. Price volatility is a possibility, because the quote is anchored to dollar strength, interest-rate moves, central-bank monetary policy and geopolitical developments.

On the plus side, gold offers high liquidity, diversification for a portfolio and a long-standing store of value that cannot be printed or conjured out of thin air, a weaker dollar further makes the metal cheaper for foreign buyers. Dollar instruments, by contrast, yield interest and are cheap to hold, yet their real return is eroded by inflation or policy-driven debasement, and they provide no hedge when the market deteriorates.

My first view of the U.S. dollar purchase was biased toward the dollar, because I discovered the dollar's liquidity to be the strongest feature and its function as the world's main reserve currency provided a feel of certainty. Yet paper money could not offer a feel of safety, the worth is not in the money itself, and I saw the buying strength of my dollar-denominated securities erode while my additional assets deteriorated during a substantial share stock downturn. I started reallocating a part of my portfolio to tangible gold and gold ETFs as a protection against economic uncertainty.. The value of my gold assets augmented during a substantial capital business decline, yet the main disadvantage I experienced was the absence of return, and the interest sometimes disappointed to surpass increasing prices. Overall, the dollar's liquidity and reserve status bring steady certainty, whereas gold provides security but no yield. The value is in the benefit each offers, and although I can exchange my assets into cash immediately, yet I witnessed its weakness firsthand.

Thomas GoldfreburgInvestor at Goldfreed

What are some tips for investing in gold and dollar?

Some tips for investing in gold and dollar are provided below.

- Some experts suggest allocation of 10-15% to gold and gold related equities is an important component of a well-diversified portfolio

- Only bullion, futures, and a handful of specialty funds allow you to directly invest in gold

- Gold oriented mutual funds and ETFs generally provide the easiest and safest way to invest in gold

- Gold futures are probably the most efficient way to invest in gold

- Gold can be invested via exchange traded fund that tracks the price of physical gold; Gold exchange-traded funds are the most liquid, tax efficient and low-cost way to invest in gold

- Gold ETFs are simple way to invest without physical ownership; Gold ETFs are the most liquid, tax efficient and low cost way to invest in gold

- Average gold investor should consider gold-oriented mutual funds and ETFs, while larger investors seeking direct exposure to the price of gold can buy gold directly through bullion

- Buy physical gold only from a certified and safe places: jewelers, gold dealers, and banks

Which option is better for you-gold or the dollar-depends on what you want the asset to do. Hold dollars in a high-yield savings vehicle if you need daily liquidity and a steady nominal value, or allocate to gold when you want a store of value that is priced as a commodity and hedges political unrest. Most investors end up using both: dollars for next-month expenses, gold for multi-year diversification. A practical middle ground is 5% in bullion or ETFs, 0-5% in gold-mining equities, and the remainder in dollar cash or short-term treasuries, review the split once a year and adjust only when major goals or risk tolerance change.

Begin with a tiny percentage to tangible gold and a high-yield reserve account plus short-term Treasury bills, handle these investments as complementary components of an entire, acknowledging their fungibility. Buy medallions from a respected vendor, for storage and coverage are critical. Create a controlled formulation to rebalancing between the two asset classes, set preset boundaries, and trade a part to recognize profits, then reinvest the payoffs into dollar-denominated instruments.

Expert behind this article

Thomas Goldfreburg

Thomas Goldfreburg is a gold investment advisor, author and founder of Goldfreed. Thomas's expertise is built on an academic foundation of a Bachelor of Science in Economics from Stanford University and complemented by market experience. Thomas specializes in gold IRA, ETF, 401k, and physical gold investments.