Fixed deposits and gold belong to different asset classes, yet both are low-risk ways that can help you build a good capital in the long run. FD offers guaranteed returns, fixed tenure options, and security of principal at maturity, while its returns are fixed and known, generally lower than other investment options. Gold investment, by contrast, typically offers a higher rate of return, has provided inflation-beating results in the past, and provides liquidity that allows it to be bought or sold easily. FD provides steady income via periodic interest payouts, is free from external factors, and can be withdrawn prematurely with a small penalty, although it carries a lock-in period. Because FD returns are generally lower, investors often weigh the safety of FD against the potentially greater reward of gold, balancing guaranteed returns with the chance of a more substantial rate of return.

Which is better: gold investment vs FD?

FD offers stability and flexible ownership, while gold value depends on market swings. Fixed deposits allow interest payout frequency choice, and longer tenure yields higher return. Gold provides indexation benefits, but FD helps inculcate a habit of dedicated savings. FD provides premature withdrawal with penalty, whereas gold can be sold as needed. Digital gold offers better benefits than physical gold, with assured purity and anytime buying or selling. Gold taxation involves capital gains tax, and gold gains receive indexation benefits. Interest from FD is taxed at your income annually. Gold is used as loan collateral, and fixed deposits are used for loans against deposits. Mix of both works best for most investors, as return depends on tenure chosen and gold price fluctuates with market factors.

Gold investment showed a varied ever-altering price, my precious metal asset moved with the market, yet during periods of significant appreciation it outpaced any FD interest I had previously earned. Gold served as a possible protection against rising prices and monetary system reduction, whereas fixed funds reassured the steadiness as the balance increased quarterly. Still, the actual value of my savings was not increasing meaningfully. Thus, the trade-off between safety and liquidity became clear: I opted for secured funds for steadiness, yet kept metal as a reserve instrument for surprising chances that arise, even if there were times of inactivity.

Thomas GoldfreburgInvestor at Goldfreed

Which provides better returns: investing in FD vs gold?

Fixed-term deposits frame their reward in a single sentence: the rate is agreed at the start, and every quarter the statement credits the same figure. NRE fixed deposits offer 6.5-7% returns, once inflation is subtracted the real surplus is about 0.5-1%, yet the nominal number is printed in black ink every time, protecting the saver from surprise.

Gold prices fluctuate by 9,800 per 100 grams (3.53 ounces) in recent weeks, in the same periods they also surged 60% this year, and last year's move was 34% upward. The metal spikes when economic uncertainty rises because global investors treat it as a reserve currency, so the holder can collect far more than 6-7% in a favourable cycle, but can equally watch the same gain evaporate when calm returns to equity and bond markets.

Over decades the upward trend remains intact, yet the ride is uneven, a household that bought at a peak and needed cash two years later has sometimes received less than the original cheque. A mix of both works best for most investors: the deposit locks a predictable slice, while gold keeps a liquid, cycle-sensitive portion that sprints ahead when headlines turn anxious.

Over the period the value of my gold investment increased, yet after calculating for rising prices the actual worth of my asset did not rise significantly. Fixed interest offered a sense of safety, as each period fixed returns was assigned to my balance, and the returns were certain. The cost fluctuated greatly, and even fell below my purchase cost, so the growth felt limited. I noted that the profits earned were moderate, whereas the value of my gold investments far surpassed the cumulative returns from my fixed deposit.

Thomas GoldfreburgInvestor at Goldfreed

Which is safer: gold investment vs fixed deposit?

Fixed deposits are low-risk investments. Having a fixed interest rate, it helps build a good corpus. Fixed deposits potentially offer more security and predictability, because they are covered under Deposit Insurance and Credit Guarantee Corporation insurance. While gold lacks organised regulation; it needs safekeeping and storage in accredited vaulting.

I thought fixed deposits were the foundation of my financial security. The returns were preset, secured, unaffected by the fluctuations I detected in other markets. I would get the accurate amount upon maturity date, this type of certainty is something I have never found in any different investments. My venture into gold investment produced a slightly different experience. The value of my investment did not rise in a stable, predictable way, and my own expectations showed its underlying unpredictability. There were periods of strong appreciation, yet there were durations of risky decline. The price of my asset grew and dropped with global market sentiment, geopolitical events, and monetary policy. Therefore, between gold investment and fixed deposit, the latter provides the greater feel of safety I sought.

Thomas GoldfreburgInvestor at Goldfreed

Which is a better hedge against inflation: FD vs gold investment?

Gold has historically served as a hedge against inflation, with its value often increasing during times of economic uncertainty. It is a tangible asset that can be held physically or in digital form, providing a sense of security. Gold prices tend to rise over the long term, making it a potentially profitable investment. However, gold does not generate income like interest or dividends. Its price can be volatile in the short term, and storage costs can be a concern for physical gold. Additionally, gold's value is subject to market fluctuations and can be influenced by various global factors.

FD's offer a fixed return over a specified period, providing predictable income. They are considered low-risk investments, especially when held with reputable banks or financial institutions. FD's are also relatively liquid, allowing investors to access their funds after a certain period, although premature withdrawals may incur penalties. The interest rates on FD's are often lower than the inflation rate, which can erode the purchasing power of the invested capital over time. FD's do not offer the potential for capital appreciation like gold or other investments. Additionally, FD's are subject to tax on the interest earned, which can further reduce the net returns.

When choosing between gold and FD's consider holding both gold and FD's in your portfolio to balance risk and return. Gold may be more suitable for long-term investment goals, while FD’s can be ideal for short-term financial needs. If you prefer stability and predictability, FD's might be more appropriate. If you can tolerate market volatility, gold could offer better long-term growth potential. During periods of high inflation or economic uncertainty, gold may outperform FD's. Conversely, in stable economic conditions, FD's might provide more consistent returns. The choice between gold and FD's should be based on your financial goals, risk tolerance, and investment horizon. Diversifying your portfolio with a mix of both can help mitigate risks and optimize returns.

Which is more liquid: investment in gold vs FD?

Gold can be sold quickly at market rates without restrictions, in contrast, fixed deposits have medium liquidity. Fixed Deposits are withdrawn prematurely with a small penalty, yet the exact ease depends on bank policies. Therefore, gold offers higher day-to-day liquidity, whereas FD liquidity is medium.

Fixed deposits were liquid assets, I submitted an easy form for early termination and money were accredited within a 24-hour interval, so liquidation was fast and penalty on the interest earned was small. When I needed quick admittance to money for medical purposes, my fixed deposits were the first source and financial aid came without delay. In contrast, ordeal with cashing my gold asset was intricate: I spent the whole day trying to find the right jeweller, and the final price depended on market rate, so my payment was fewer than the initial buying cost.

Thomas GoldfreburgInvestor at Goldfreed

Is FD or gold investment better for diversifying your portfolio?

Portfolio diversification is achieved by adding fixed deposits, because an FD scheme generates a secondary source of income that is largely insulated from market swings. Yet most funds must not sit in one asset, a portfolio includes gold alongside FDs so that the two instruments cover different risks. Gold is known to do well during market lows, and its low beta cushions equity shocks, while FDs provide portfolio diversification through predictable interest. Investors can buy or sell gold anytime, either as physical gold, sovereign gold bonds, or gold-backed ETFs, so the position can be trimmed or enlarged without waiting for maturity. In contrast, premature withdrawal from an FD typically incurs penalties, making the slice of the portfolio parked in deposits less flexible once booked. Therefore, the better diversifier is the pair, not either alone: allocate the core stabilising portion to FDs and overlay it with gold, bought as a commodity or through ETFs, so that steady income and counter-cyclical strength coexist in the same portfolio.

My gold investment contrasted with the static function of my fixed deposits, because its price moved with the economy, whereas the price of the fixed venture was not changed. I noticed that gold investment conducted comfortably during times of economic uncertainty or inflation. I reallocated a little part of my savings to sovereign gold bonds, and this offered a reassuring foundation for my assets. Therefore, combining the certainty I recognized from fixed deposits with the inflation-hedging capacity of gold created a balanced diversification.

Thomas GoldfreburgInvestor at Goldfreed

Which is taxed more: gold or FD investments?

Gold futures funds have a top federal tax rate of 26.8%, and funds that hold gold futures contracts are structured as partnerships and issue a K-1 tax form. Physical gold is a collectible with long term capital gains tax maximum is 28%. Gold ETFs are also reviewed as collectibles, and there is no getting around that collectibles rate just because it is held in an ETF cover. Exchange Traded Funds rate of taxes is 20% plus a 4% cess for long term capital gains, yet both long and short term gains from these investments also get hit with the 3.8% NIIT and state income taxes.

Interest earned on a fixed deposit is taxable as per the current income tax rates, and FD interest is taxed annually as per income slab rates. Fixed deposits have a tax saving option under Section 80C, but the interest on fixed deposits is taxed as per the current income tax rates. Consequently, gold futures contracts have a higher statutory capital gains burden than FD interest, while FD interest is taxed as ordinary income at the investor's marginal slab rate.

What are the pros and cons of investing in gold and FD?

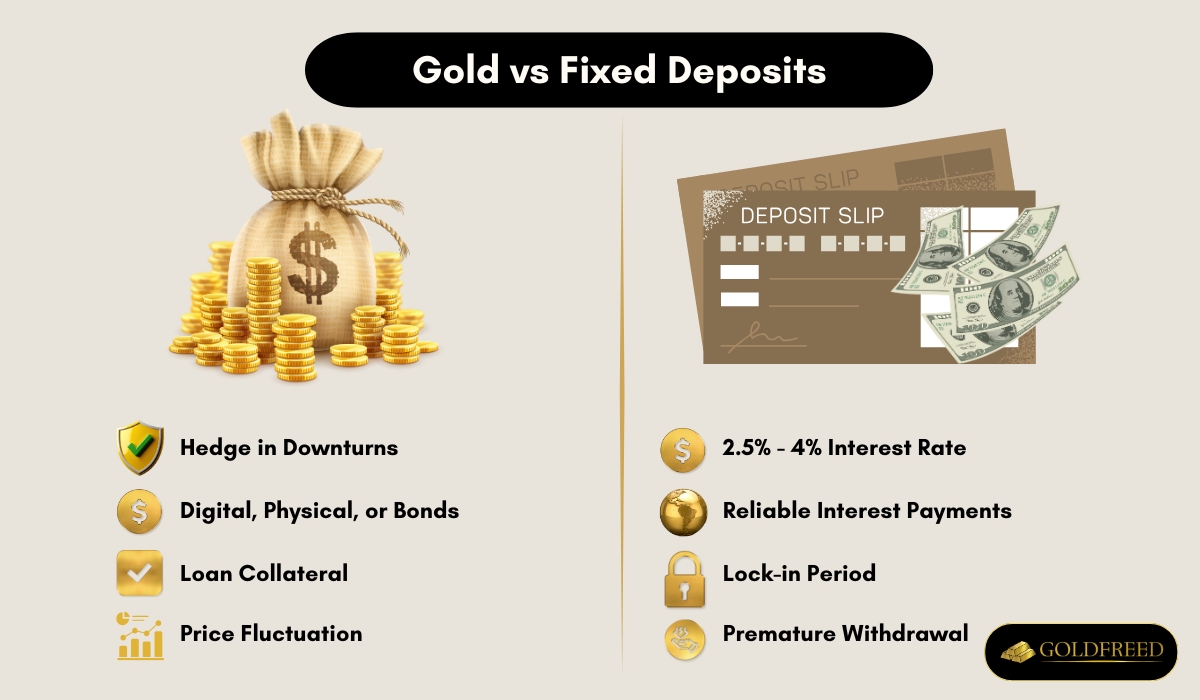

Gold provides long-term appreciation and rises during economic downturns, offering a hedge when other assets fall. It is bought digitally from 1, stored physically, or held as Sovereign Gold Bonds, and sold anytime in the market for cash quickly. Banks and NBFCs offer loans against gold up to 80% of value, and gains held beyond three years benefit from 20% tax with indexation. Yet gold does not give regular income, price fluctuation is moderate to high, and physical holdings incur locker rental charges.

Fixed deposits in the UAE pay steady interest income of 2.5%-4% per year, with senior citizens receiving higher rates, longer tenure leads to higher return. The deposit does not require storage, takes monthly or quarterly interest payouts, and serves as loan collateral up to 80% of value. However, fixed deposits have a lock-in period and premature withdrawal incurs penalties, breaking the deposit early, whether through paperwork or simple request, will reduce overall earnings.

Fixed deposits provided a reassuring feel of safety, I valued the certainty and appreciated the secured payments, while the procedure was straight and required minimal efforts on my part. Gold supplied an important protection during times of economic uncertainty. Yet the cost of gold can fluctuate sharply (falling or stagnating), so the primary drawback I experienced was the inherent volatility. Meanwhile, the actual amount of my fixed deposits returns felt like a fast deflation of my purchasing power, the actual worth of my returns was minimal because I earned interest and struggled to keep up with inflation.

Thomas GoldfreburgInvestor at Goldfreed

What are some tips for gold and FD investment?

Some tips for gold and FD investment are provided below.

- Use an investment account like a brokerage account or IRA for gold ETFs

- Take advantage of low minimum investments and low-cost exposure via ETFs

- Use gold ETFs or mutual funds as the simplest way to invest without physical ownership; consider using gold ETFs backed by physical storage like GLD

- Before investing, monitor geopolitical factors and central bank activities

- Allocate 5% to 10% of a portfolio to gold

- Buy digital gold through reputable dealers

Investors who prefer direct exposure can buy physical bars or coins from reputable dealers or take delivery from certain ETFs, whereas those comfortable with derivatives can use gold futures, which allow leverage and are the most efficient vehicle for speculating on gold rising or falling. ETFs track the price of gold, are backed by physical storage such as GLD or SGOL, can be bought and sold like a stock, and require smaller dollar amounts than bullion while sparing investors the need to store physical metal securely. For fixed-income allocation, keep FD maturities staggered so that deposits mature at intervals and are rolled over at prevailing rates, and assure that cumulative balances across banks stay within the insured limit. Whenever rates are rising, prefer short-tenure FDs so that renewal captures higher coupons, while in a falling-rate lock in long-tenure FDs to preserve yield. Finally, compare post-tax returns: if you are in the highest tax bracket, review 5-year tax-saver FDs for the deduction, but otherwise favour regular FDs or recurring deposits whose interest, though fully taxable, helps budget for systematic goals.

My personal voyage with gold and fixed deposits started with a clear purpose: gold for long-term strategy, and FD as foundation of my financial safety. I did not buy gold during market peaks, instead, I waited for value corrections to produce my assets.

Thomas GoldfreburgInvestor at Goldfreed

Which option is better for you: investing in gold or FD?

For anyone whose monthly income is fixed, fixed deposits provide convenience that gold cannot match. The amount, tenor and post-tax return are known on the day the deposit is opened, no price-chart has to be watched, no locker rent has to be paid, and premature encashment is only a few clicks away because fixed deposits are digital. In the same tenor, therefore, FDs stand stronger against the twin risks that worry small savers-price volatility and liquidity shock.

Yet both options have their own advantages and disadvantages. Gold protects during inflation, it is pledged for an overnight loan, and carries emotional weight. A mix of both works best: keep three-to-six months of planned expenses in an FD ladder for certainty, and hold a small, ring-fenced quantity of gold for the unlikely year when everything else falls.

Protection against inflation mattered when I started exploring gold investment, yet it does not generate earnings. Fixed deposits provided total assurance and guaranteed returns. Short-term goals encompassed keeping a down deposit, so I assigned part of my funds in FD where the risk to the principal was zero. I could not afford volatility, and this confidence encouraged my short-term goals and strengthened my financial status. Over a long period, purchasing ability of gold maintained buying strength. My investment scope expanded only after I gained total confidence in the steady cornerstone of deposits, thus, for near needs, I chose fixed deposits, and for long-term stock of worth I keep gold investments mainly through sovereign gold investments.

Thomas GoldfreburgInvestor at Goldfreed

RD vs gold investment: which is better?

Recurring deposits lock money into a fixed schedule, pay known interest, and create no surprise, gold offers lower entry costs and a story as old as civilization itself. A recurring deposit suits savers who want certainty, yet it cannot beat inflation if rates lag. Gold collapsed by 33% during the Great Financial Crisis and swings 20% in a quarter, so the saver must stomach price noise.

Since 2000, gold's price has outperformed Warren Buffett's Berkshire Hathaway by 133%, a statistic that lures many, yet advisors think belief in gold is misguided if the horizon is short. Real wealth is built through intentional diversification, therefore, some investors hold both assets. Those who need a forced-saving habit and guaranteed capital can choose the RD, those who accept volatility and want a tangible hedge allocate monthly surplus to gold instead.

Appreciation in the gold's value outpaced my recurring deposits, yet the worth of my venture enjoyed substantial variations that were unsettling compared with the steady rhythm of my RD. Periodic contributions imposed financial control and the security of the corpus sum was reassuring, I recognized guaranteed restore, but growth potential was restricted. Although this asset provided an important protection against rising prices, my fixed-income investments could not accomplish real growth, for post-tax incomes hardly kept pace with inflation. I valued the disciplined approach of my RD, while my recent entry into gold showed a volatile dynamic that made me wonder if it was the efficient vehicle for my financial goals.

Thomas GoldfreburgInvestor at Goldfreed

Which provides better returns: RD vs gold investment?

Gold investments have better returns, but they are prone to market risks, whereas fixed deposits are more secure against fluctuations and provide guaranteed returns, though they have lower returns.

Recurring deposits lock the money at a fixed coupon, so the maturity amount is known on the day the first instalment is deposited, gold's value, in contrast, depends on market swings. Over the last five years, gold ETFs have generated a cumulative return of 5.37%, while the surge in gold prices over the past year has lifted the metal's annualised return closer to eight percent. Yet this out-performance is episodic: gold price fluctuates in the short term because it is related to factors like inflation, import duty, trade relations and supply of gold, and the asset does not generate passive income. RDs, assured but capped, normally offer 5.5-6.5% post-tax, gold beats that when the cycle turns, but it under-performs for long stretches with a 70% chance. Therefore, if the comparison is framed strictly around better returns , gold wins in years of macro stress, while RDs win in calm years, making the choice a timing decision rather than an absolute one.

My venture into gold investment was mainly through a Sovereign Gold Bond program, where returns gave a secured principal and the potential for capital appreciation. Over a longer horizon the appreciation was considerable and far exceeded the payments from my recurring deposit. I started my journey with recurring deposits, the efficient return was low, yet the proceeds were stable. Over a five-year term the proceeds were precisely as planned by the bank, but the growth did not outpace inflation.

Thomas GoldfreburgInvestor at Goldfreed

Which is safer: recurring deposit vs gold investment?

If you want security and stable income without major risks, term deposits are a better choice for long-term investment because they provide fixed returns. Gold is a liquid investment that carries risks but could be the right choice if you want to invest money for long-term returns.

If safety means capital protection and predictable reward, the recurring deposit is safer. Deposits have a fixed tenure, the bank sets the interest rate at the time of opening the account, and at maturity the principal plus interest is guaranteed. In contrast, gold prices fluctuate significantly, global economic factors, currency exchange rates, or monetary policy push the price down, so the original money is not assured.

Yet safety also means access at the moment of need. Here gold offers more flexibility: you can sell gold whenever you want, whereas deposits have fixed lock-in period and early withdrawal incurs penalty. Therefore, while deposits protect nominal value, they are inflexible and not suitable for emergency funds, gold carries market risk but converts quickly, so the saver must decide whether the priority is shield or speed.

I considered recurring deposits a safer choice. My RD is not risky, and the total corpus is protected. My RD has never made me worry about losing my venture. I know precisely how much my money will increase over the particular term, because it is guaranteed by the bank. My experience with gold investment has been different. Although I have seen the value of gold grow significantly, volatility creates a risk. The market price fluctuates, based on worldwide economic factors, and sudden drops delete paper profit. I have seen steep declines. Therefore, between recurring deposit and gold investment, I consider the former the safer option.

Thomas GoldfreburgInvestor at Goldfreed

Which is a better hedge against inflation: RD vs gold investment?

Gold is a hedge against inflation, increasing in value as the purchasing power of the dollar declines. Treasury Inflation-Protected Securities (TIPS) provide built-in inflation protection, and government bonds have shown to pay higher rates when inflation rises.

Between a recurring deposit and gold, the metal is the stronger inflation shield. Gold protects purchasing power over long periods, while an RD fixes both the sum and the coupon. A single RD therefore never rises with prices.

Gold, in contrast, is a commodity, and commodities outpaced inflation in all five periods shown. The distinction shows up in history: gold lost nearly four-fifths of its real value between 1980 and 1999, yet over full inflation cycles it still preserved more real value than any nominal deposit. An RD gives certainty of capital but no escape from rising prices, so gold, despite its own volatility, works better as a long-run inflation buffer.

The recurring deposit failed as an efficient hedge, the interest yielded was less than the prevalent rising prices charge. I recognized my monetary funds were growing numerically, yet I saw their true purchasing power was decreasing, my wealth was losing power over duration. The price of gold mostly grew over a period, its cost appreciation significantly outpaced rising prices. I bought these bonds during a time of economic uncertainty and increasing consumer price, and my move into gold produced a varied result, but its return was not overtaken by the eroding impacts of inflation on my money.

Thomas GoldfreburgInvestor at Goldfreed

Which is more liquid: RD vs gold investment?

Gold is a liquid asset because it can be bought and sold at any time without waiting for a fixed term to end. Gold has the largest and most liquid market among precious metals, with daily trading volumes averaging around US$233 billion. Gold ETFs trade like stocks during exchange trading hours, so they are redeemed more easily and do not carry exit loads. Digital gold and paper gold through ETFs provide cost-effective, liquid alternatives to physical gold, removing storage risk and allowing investors to sell gold anytime in the market. In contrast, recurring deposits lock money for a set tenure and impose penalties for early withdrawal, making them far less liquid.

I discover recurring deposits are more available than precious metal. The procedure for taking out money from an RD is straightforward and predictable, virtually every financial institution permits me to terminate the RD prematurely with a little penalty. This offers me a definite conception of when I will get the whole capital and interest, which is automatically attributable to my funds balance upon the due date. In contrast, my experience with gold assets shows a liquid operation only when I hold Sovereign Gold Bonds or digital precious metal. Yet, if I possess gold metal jewelry or coins, I have to change them into currency, so I must start to find a good purchaser. I am reliant on market situations to obtain a favorable value, and the amount I get often includes deductions for purity and a service fee. Therefore, I regard the liquidity of my assets as higher with an RD, because its timeline and value are fixed, whereas the value I get from gold is subject to the current market cost.

Thomas GoldfreburgInvestor at Goldfreed

Is RD vs gold investment better for diversification of your portfolio?

Gold offers protection and diversification because it moves to the beat of its own drum, untied to corporate earnings or interest-rate policies. A recurring-deposit block, by contrast, is chained to the bank's fixed rate and therefore amplifies portfolio concentration risk instead of reducing it. When you spread your money between gold bullion-rounds, bars, coins, ingots-and a basket of short-maturity debt instruments, you create low-correlation positions that offset losses in stocks. Investors can buy gold bullion directly or hold it indirectly through low-cost passive index funds: the iShares Gold Trust (IAU), either route delivers genuine diversification.

Yet the promise of diversification collapses if you over-allocate to one metal or over-diversify into dozens of similar deposits. A balanced mix of gold and debt diversification is usually enough, adding real estate or passive index funds/ETFs further stabilizes the portfolio without tipping it into ineffective over-diversification. Rebalancing, the primary part of portfolio management, keeps the weight of gold and the scheduled RD cash-flows at the target level, assuring that the portfolio retains both protection and liquidity across market cycles.

I allocated a part of my funds to a recurring deposit and began a Systematic Investment Plan in precious metal ETFs, realizing the necessity for diversification. The RD offered predictable simple growth and guaranteed payments, while the steady interest rate gave a feel of safety. My gold assets gave a precious counterweight during downswings, acted inversely to the market, and served as important protection against geopolitical uncertainty and rising prices. This element of my portfolio was untouched by market volatility and performed as a steady mainstay, whereas compelled periodic contributions assisted me in developing my financial portfolio.

Thomas GoldfreburgInvestor at Goldfreed

Which is taxed more: gold or RD investments?

Physical gold and other precious metals are deemed collectible in the tax code, so long-term gains are taxed at a top 28% rate. Sovereign Gold Bonds sold in the secondary market before maturity face long-term capital gains at 20% with indexation or 10% without, whichever is more beneficial, yet both long- and short-term gains from these investments also get hit with the 3.8% NIIT and state income taxes.

Recurring-deposit interest, by contrast, is taxed as ordinary income each year, so the rate reaches 37% at the federal level, well above the 28% collectibles cap. Net short-term capital gains on gold held one year or less are likewise taxed as ordinary income, but once the holding period crosses one year the 28% collectibles rate caps the federal bill, whereas RD interest has no such ceiling. Thus, for taxpayers in the top bracket, RD income is normally taxed more heavily than long-term gold profits, while short-term gold gains and RD interest are taxed identically at ordinary-income rates.

What are the pros and cons of investing in gold and RD?

Gold adds balance and provides a hedge in a potential economic or market downturn, yet it does not generate regular income. Physical gold requires secure storage and incurs dealer commissions, insurance, and storage costs, hence gold has high investment cost. Gold ETFs provide exposure to gold without storage responsibility, but they have expense ratios. Gold price rises during periods of market stress, currency instability, or geopolitical tension, yet gold price falls when the economy is strong. Gold turns a small amount of money into a large gain, yet gold also turns a small amount of money into a large loss because losses are magnified with smaller price movements.

Recurring deposits (RD) offer predictable returns and steady accumulation through small monthly installments. RD does not require storage or insurance, nor is it exposed to price volatility. The return is fixed, so there is no potential for outsized gains, yet the capital is protected and no loss is magnified.

Investing in gold offers a unique feel of peace because its price frequently rises when stock markets are unstable, yet its value can also change for long durations and it locks up my principal without any return. The substantial disadvantage is the absence of steady cash flow: my gold assets do not produce returns, I must constantly view the expenses related with producing and dealing active precious metal as well as fears about safe storage. In contrast, the unchangeable percentage rate of a recurring deposit assures that I realize precisely how much money I will get at the due date, giving total assurance of proceeds that is ideal for designing specific financial aims. I value the controlled saving practice of RD, even though the interest yielded frequently hardly surpasses rising prices, so the true growth of my funds is modest.

Thomas GoldfreburgInvestor at Goldfreed

What are some tips for gold and RD investment?

Tips for gold and RD investment are provided below.

- Allocate 5% to 10% of a portfolio to gold, limiting gold exposure to less than 3% of one's overall portfolio.

- Use a brokerage account to hold gold-related investments.

- Use gold ETFs, mutual funds for low-cost, low-minimum investments or gold mining stocks for effective profit.

- Combine technical analysis with leveraged products for gold investing; monitor strategic market timing, crucial for maximizing gold investment returns.

- Choose the right type of gold investment: gold futures, a Gold IRA, or leading gold ETFs like SPDR Gold Shares (GLD) and iShares Gold Trust (IAU).

- Purchase physical gold bullion through reputable dealers or collectors.

- Buy physical gold bars and widely circulated coins for direct ownership.

ETFs and mutual funds that track the price of gold offer the simplest, lowest-cost route: shares can be bought and sold like stocks through any brokerage account or IRA, require smaller dollar amounts than bullion, avoid storage headaches, and still deliver full exposure to gold price movements. Popular choices include SPDR Gold Shares (GLD) and iShares Gold Trust (IAU), both backed by physical bullion vaulted in jurisdictions with strong property rights. Investors who prefer tangible assets can purchase widely circulated coins, bars, or rare collector pieces from reputable online dealers or storing them in vaults. For those comfortable with equity risk, gold mining stocks provide leveraged participation because profits rise faster than bullion prices, yet miners are tied more to business fundamentals than to the underlying commodity, so only established producers are added after rigorous technical and operational analysis, junior miners carry higher risk. Executing strategic market timing is vital for maximising returns in gold investing, but most savers will fare better with a disciplined, small allocation purchased at regular intervals rather than attempting to call every cycle.

On the recurring-deposit side, treat the RD as a compulsory cash-flow tool: schedule the instalment to coincide with salary credit so the default rate stays near zero, pick a tenure that matches your next big cash need (school fees, down-payment, festival spending), and instruct the bank to sweep the maturity proceeds into a short-term FD instead of a low-yield savings account. Avoid step-up RDs that tempt you to double installments later unless your income is genuinely predictable, missing even one payment resets interest to the lower savings-bank rate. Finally, insure the primary income earner so the RD does not stall under unforeseen shocks, and review the combined gold-plus-RD bucket once a year-raise the gold ETF weight only if geopolitical stress or central-bank buying intensifies, otherwise keep the RD growing steadily to anchor the plan.

I control my RD contributions as a non-negotiable monthly expense, like a service invoice, and keep the tenure aligned to the goal. The 36-month RD matured precisely when I required the funds. I have found RD useful for specific short-to-medium-term financial objectives. Furthermore, I allocate only a small portion of my part to gold, because I review gold assets as a long-term protection against inflation, and buy SGBs regularly during new issuances to average the price. In addition, I found Sovereign Gold Bonds a useful method that removes storage concerns and gives an annual percentage, whereas physical gold offers no yearly return.

Thomas GoldfreburgInvestor at Goldfreed

Which option is better for you: investing in gold or RD?

If you value flexibility and market-linked upside, gold ETFs are certainly easier to buy, hold, and sell than a bank recurring deposit. A gold ETF can be bought through an online broker just like a stock, needs no locker, and its price is linked to the price of gold, so you gain when the metal rallies. In contrast, an RD locks you into a fixed rate and tenure, early exits invite penalties and the return is capped. Gold ETFs do not generate income like dividends, yet they are more cost-effective than physical gold, which includes dealer commissions, sales tax, and storage hassle.

On risk, gold ETFs are subject to market risk and follow supply and demand indices, whereas an RD carries near-zero credit risk with scheduled banks and is immune to price swings. If you crave certainty of capital and cash-flow discipline, the RD's predictable monthly instalment and assured maturity value win. If you seek inflation hedge and liquidity, gold ETFs give investors exposure to gold without having to directly purchase, store and resell the precious metal. Choose RD for safety and forced saving, choose gold ETFs for flexible, low-cost gold exposure.

Gold lacks the stable yield of an RD, yet it offers potential for capital during periods of economic uncertainty. RD fit my requirement for an easy, low-maintenance savings method, the fixed monthly contributions and secured proceeds at due date gave me a feel of safety and confidence, making it easy to plan for specific goals. I appreciated the certainty, realizing precisely how much I would gain at the end of the term, whereas gold remains a protection against inflation and monetary instability.

Thomas GoldfreburgInvestor at Goldfreed

Expert behind this article

Thomas Goldfreburg

Thomas Goldfreburg is a gold investment advisor, author and founder of Goldfreed. Thomas's expertise is built on an academic foundation of a Bachelor of Science in Economics from Stanford University and complemented by market experience. Thomas specializes in gold IRA, ETF, 401k, and physical gold investments.