Diversifying between gold and life insurance balances security with growth: life insurance offers tax advantages and investment flexibility, while gold preserves value against inflation. Life insurance creates a dependable legacy, yet gold grants great liquidity. Weighing these distinct benefits clarifies which asset, or blend, best fortifies your long-term plan.

Expert behind this article

Thomas Goldfreburg

Thomas Goldfreburg is a gold investment advisor, author and founder of Goldfreed. Thomas's expertise is built on an academic foundation of a Bachelor of Science in Economics from Stanford University and complemented by market experience. Thomas specializes in gold IRA, ETF, 401k, and physical gold investments.

Which is better: life insurance or gold investment?

The answer lies in how each vehicle behaves under stress, how it compounds, and how easily it can be converted to cash without surrendering the asset itself.

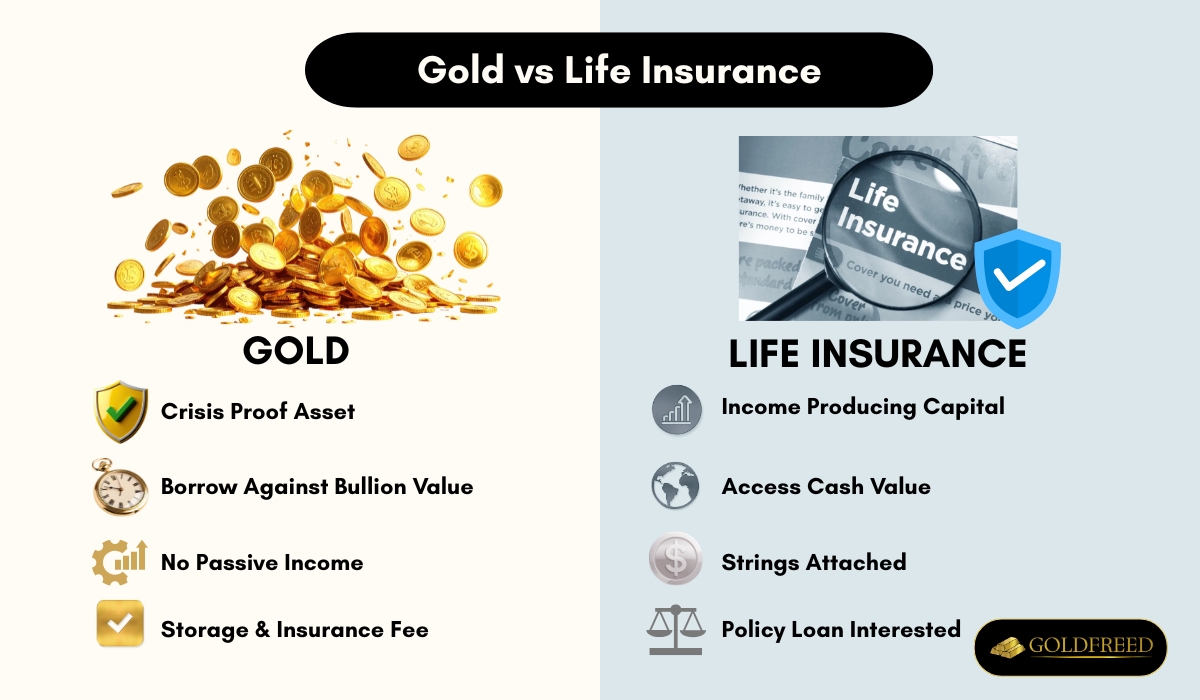

Gold has performed better in times of crisis, yet holding physical gold doesn't generate passive income and gold price rarely correlates with stable growth. Gold investment companies let you borrow against gold bullion value without selling holdings, so borrowing against gold bullion provides liquidity, still, the underlying asset merely sits in a vault.

Life insurance offers flexibility through the Family Bank Strategy, which leverages the cash value of your whole life insurance policy to create a source of private capital. You can borrow against your policy's cash value, and borrowing against cash value takes advantage of its long-term appreciation. Loans or withdrawals from whole life insurance are possible but often come with conditions, even so, the strategy allows you to hold cash value in your policy and to redeploy it at will. In this way, Infinite Banking allows use of cash value of whole life insurance policy, making it not only a reliable wealth-building tool but truly better than gold.

Pairing gold with Infinite Banking provides the best of both worlds: crisis-proof bullion and income-producing, liquid capital. The final choice depends on investor profile and financial goals.

Life policy supplied an unequivocal security net, precious metal lacks the defensive nucleus of living policy. Gold functions as a high-riskinvestment for possible asset growth, yet its price fluctuates significantly based on market demand. Life insurance is not a venture in the traditional sense, but the guaranteed value brings a steady feeling. Gold provides a tangible appearance of wealth.

Which is riskier: life insurance or gold investment?

Gold is reviewed as a safe investment, especially in times of crisis, whereas life insurance offers flexibility and attractive tax advantages; therefore, you benefit from the advantages of each type of investment.

Gold is a lower-risk investment overall, especially for the medium to long term, because gold is not positively correlated with stocks, bonds, or real estate, so adding gold reduces overall risk in a portfolio. Life insurance has very low risk with reputable insurers because it guarantees a payout to beneficiaries upon the policy holder's death, and a whole life insurance policy has cash value that can grow uninterrupted at a set interest rate without risk of loss. Therefore, gold is riskier than life insurance in terms of price volatility, yet life insurance is lower-risk in terms of guaranteed outcomes.

Life insurance carries peril only in the prospect of my untimely death, this danger is tied to my own life conditions and is wholly within my grasp, since I pay a fixed amount each year and obtain the guarantee that my household would be financially secured. Gold investment, by contrast, was a volatile ordeal: the worth of my precious metal holdings was in a continuous alteration, determined by worldwide economic, geopolitical events and monetary forces I could neither predict nor influence. Therefore, gold investment is the riskier choice, while life insurance remains a plain, certain deal.

Thomas GoldfreburgInvestor at Goldfreed

Which is a better protection against inflation: investing in life insurance vs gold?

Gold is often hailed as a hedge against inflation, yet its record is mixed. Over the last forty years gold showed zero correlation with inflation, making it less effective than many assume. Commodities and precious metals have provided protection against unexpected inflationary shocks, but they carry a lower batting average of outperforming inflation. Gold takes the lead only when inflation jumps above 8% yearly, below that threshold real estate historically outperforms gold during low to moderate inflation. Japanese insurers therefore regard real estate, REITs, and equities related to living expenses as more natural inflation-hedge choices, finding gold not compelling enough on its own.

Storage differences reinforce the tilt toward bullion alternatives. Physical gold requires secure vaults or safe-deposit boxes that incur annual fees, while life insurance is a paper contract with no storage cost. Because commodities often rise in price with inflation, funds that hold futures or ETFs offer inflation protection without the burden of holding bullion. Stocks offer protection against inflation through growth potential and dividends, and an S&P 500 index fund provides long-term attractive returns that beat out inflation. A well-diversified portfolio that blends equities, real estate, and Treasury Inflation-Protected Securities provides long-term attractive returns that beat out inflation more reliably than an isolated position in gold.

Gold historically maintained its buying strength, so I regard precious metal as a timeless store of value. Though its price was subject to monetary variations, I felt the unpredictability inherent in precious metal costs. Because genuine security against rising prices comes from the contract's secure guarantee, I allocated a part of my reserves to an entire life insurance. Cash value was mostly segregated from stock exchange volatility, and death benefit is a specified guaranteed amount.

Thomas GoldfreburgInvestor at Goldfreed

Which is easier: investing in life insurance vs gold?

Opening a life-insurance policy is usually a one-meeting or online formality, once the premium is fixed, the policy runs without further action from the investor, and the insurer handles all administration. Gold, by contrast, obliges the buyer to secure a vault or to pay recurring storage costs, and every sale or purchase demands verification of weight, purity, and price. Because liquidity is limited for both assets, the simpler structure belongs to life insurance: paperwork replaces safes, and the flexibility of scheduled premiums replaces the need to guard physical bars.

My first attempt at gold assets was far complicated. I choose between tangible gold coins and digital alternatives like sovereign gold bonds. Acquiring a tangible resource meant tracking fluctuating buy-sell costs and confirming authenticity. Physical gold possession also demands safe storage. I explored respectable vendors and provided required papers, and I learnt the subtleties of purity. My way into life insurance started with a direct online program. Simplicity of setting up autoloading payments clarified the long-term commitments. Contractual conditions outlining my payments, and I passed a routine health check. A representative reviewed my medical record and communicated with me. I obtained a contract tailored to my needs. The whole process was organized, secure, and easy.

Thomas GoldfreburgInvestor at Goldfreed

Which offers higher returns: life insurance vs gold investment?

Comparing life insurance returns and gold, life insurance offers stable long-term growth, while gold has often performed better in historical crisis times.

Gold had average annual returns of 10.6% from January 1971 to December 2019, recent history shows gold had over 23% annual growth in 2020. Gold has shown steady returns in the past decade, yet gold returns depend on the period under consideration. Gold offers spectacular returns in times of crisis, and gold returns are better when real interest rates are low or negative. Cash value life insurance gives one of the lousiest returns, Tata AIA Life Insurance offers an insurance plan which provides attractive market-linked returns, yet market-linked returns fluctuate with it. Higher interest rates make gold less attractive, gold does not pay interest and gold does not pay dividends, so passive income is absent.

The choice depends on your financial goals and your investor profile.

The monetary growth of the policy insurance's cash value is sluggisher than possible gold investment returns. The proceeds from my life policy scheme were not the same volatile as precious metal. The worth of my precious metal possessions sometimes gave spectacular returns during times of economic uncertainty. These gains are subject to external industry pressures. These profits are not promised. The price of my precious metal properties have fluctuated with worldwide business situations. The financial growth of the policy insurance's cash is cautious. The contract offers a secured amount guaranteed to my beneficiaries.

Thomas GoldfreburgInvestor at Goldfreed

Which is taxed more: life insurance vs gold investment?

Gold is classified as a collectible by the IRS, so gold held for more than a year is subject to long-term capital gains tax at your marginal income tax rate, up to a maximum of 28%. If you hold your gold for less than a year and sell it at a profit, you'll be taxed at regular income tax rates, short-term capital gains on gold are counted as ordinary income.

Life insurance benefits from advantageous taxation. Under IRS Section 7702, all realized gains and income that occur within a life insurance policy are not taxable, and all proceeds are income-tax-free to the beneficiary at the insured's death. After eight years of ownership, the policy owner can take tax-free withdrawals and loans from the contract.

Therefore, gold investments are taxed more heavily than life insurance, especially when profits are realized quickly or when the 28% collectible rate applies.

Death benefit is generally received free of income tax. Cash value increases on the tax-deferred part, so I am not taxed on profits each year. Gold investment is subject to taxation, profit is assessable in the year of sale and is typically dealt as capital gain, therefore the tax consequence reduces my total proceeds.

Thomas GoldfreburgInvestor at Goldfreed

What are the pros and cons of investing in gold or life insurance?

Investing in gold delivers high liquidity and acts as a portfolio diversifier, adding balance and security by hedging against market volatility, crises, and geopolitical uncertainty. It is stable and serves as a safe haven when stocks and bonds tumble. Yet physical gold does not generate passive income and incurs storage and security costs that erode gains, storage is expensive and requires budgeting for insurance as well. Gold ETFs present a cost-effective alternative with lower transaction costs, while gold stocks can earn dividends, though they do not offer the same features as holding bullion.

Life insurance, in contrast, offers flexibility and builds cash value that grows tax-deferred and can be withdrawn or borrowed against with certainty. Annuities within policies assure consistent income through guaranteed payments, providing a degree of certainty. Nevertheless, premiums are massive and management fees apply, so investors must compare investment options carefully. By blending gold's liquidity and diversification with the deferred growth and income certainty of life coverage, a household can balance security and growth without over-committing to either asset.

Life coverage insurance gave peace of mind. I allocated a part of my financial to life insurance policy, and the required system of rules of regular payments worked as an organized form of savings. Yet I discovered that the proceeds from conventional death benefit insurance were small, compared with other financial vehicles, so I saw substantial disadvantages. Gold performed greatly during times of economic uncertainty, which is an effective counterbalance to the volatility of my other assets. However, gold does not offer profits or income, and its risk reduction cannot replace those of life insurance. The purchase procedure and storing tangible physical gold involved extra expenses. Gold price is subject to market trends, and industry cost increase can cause stagnation durations.

Thomas GoldfreburgInvestor at Goldfreed

What are some tips for investing in gold and life insurance?

Tips for investing in gold and life insurance are provided below.

- Investors should regularly review and rebalance portfolio including gold investments

- Financial advisors recommend keeping a maximum of 5-10% of portfolio in gold

- Regularly reviewing and rebalancing portfolio including gold investments is important

- Progressive investment starts with small portion of gold and gradually increases over time

- Choosing the right life insurance policy is essential if integrating insurance with long term planning

- Storing gold somewhere safe is important for protecting your assets

- Gold ETFs allow investors to avoid biggest risks of owning physical gold

Gold is bought via gold ETFs, mutual funds, physical gold, futures, or specialty funds, each option has different implications for storage, costs, and investment flexibility. A gold, ETF or mutual fund is the simplest way to invest in gold, because gold ETFs offer low-cost exposure with low minimum investments. ETFs are bought and sold like stocks while they track the price of gold. Investors can buy gold bullion which is physical gold:coins, bars, ingots. Though physical gold requires storage and insurance fees, so keep gold bars and coins in a safer protected place like a bank safe deposit box. Gold futures are probably the most efficient way to invest in gold, yet they demand an investment account and higher risk tolerance. Gold mining companies are another investment option, but gold mining stocks don't always track gold's long-term performance. If you seek an objective store of value that hedges currency risk, allocate 5-10% of the portfolio to gold and store it safely. Many investors combine both: they insure themselves with their whole life, accumulate cash value, borrow against it to buy gold ETFs or coins, and regularly review and rebalance the blended portfolio.

For gold, start with a tiny controlled purchase and allocate a fixed quantity each year towards sovereign gold bonds, valuing them for further benefit and security. I view gold as an important portfolio diversification, giving security during economic uncertainty, yet it is not the main source of rapid gains generated. For life coverage, think about upcoming financial needs, and choose a simple condition scheme for the proper coverage amount. Choose a basic term program at reduced charge, guaranteeing maximum security. The key for both assets is consistency and a long-term perspective.

Thomas GoldfreburgInvestor at Goldfreed