Gold has been outperforming the S&P 500 in 23 of the past 54 years, delivering a 9-multiple while the index delivered 6 . During the 20-year and 5-year windows, gold beat the S&P 500 by an average 20.5 % in the index's negative years, and it rose in eight of nine calendar years when stocks fell. Because gold is a safe-haven asset, its price climbs when economic uncertainty climbs. Investors buying gold due to uncertainty treat the metal as diversification that has a more stable value than stocks. Yet gold has no income from dividends, so gold investors risk losses if the price stalls, whereas S&P 500 investors buying stocks participate in corporate growth and periodic cash payouts.

Is gold investment better than S&P?

S&P has a better historic record of yield than gold. $100 invested in 1971 became $36,104.55 for the S&P 500, while the same stake in gold reached $7,023.46. With yield, gold achieves $33,687.86, yet the compound advantage still favors equities. Gold is up over 60% so far in 2025, yet this spike is a short-term jolt, not the slow compounding that allowed the S&P 500 to multiply sixfold from 2000 to the mid-2020s. When negative, the S&P 500 averaged -15.3%, a reminder that its downturns are sharp but finite, whereas gold's ninefold multiplication across the same two decades came in sporadic surges that left long gaps of flat prices.

Gold therefore offers a tactical hedge, not a strategic replacement. Its 62% YTD leap shows it can sprint, yet over half-century stretches the index's reinvested dividends still outpace the metal's glow.

Gold functions as a type of financial protection, moving independently of the stock exchange during times of economic uncertainness or heavy stagflation. The S&P 500 constitutes a wager on corporate gain and profitable advancement. The combination influence of reinvested profits and the intrinsic innovation within the American system have demonstrated to be a strong wealth-building instrument over the lengthy range. I do not believe one venture inherently better than the opposite as they do have varied strategy goals. My assignment to precious metal provides a varied function, and it has worked as a stabilizer.

Thomas GoldfreburgInvestor at Goldfreed

Is gold investment better than the stock market?

The answer depends on the era you measure and the function you want the asset to play. Over the 30-year window that ended in 2020, gold increased 360%, a figure that rivals the long-term gain of equities but arrived with a very different ride. Stocks generated an annualized total return of 10.6% from 2004 through 2024, while gold delivered its strongest bursts during crises when demand for gold rises and the price goes up. These episodes remind investors that gold is a store of value first and a growth engine second.

Gold provides a counterbalance to stocks because its value tends to move inversely to the stock market. When investors' attention shifts to stocks, the gold price tends to fall, and vice-versa, a rhythm that lowers overall portfolio volatility. Gold ETFs and gold miner stocks are effective tools for capturing this diversifier without the need to store coins or bars. Although the metal is volatile in the short term, its low correlation to equities has made gold a more robust diversifier than silver or commodities tied to industrial cycles.

Ownership in companies that have the potential to grow and generate profits remains the central attraction of equities. Gallup respondents still thought stocks or mutual funds were the best long-term investment even after a six-percentage-point decline from 2024. Yet the same survey period reminds us that the stock market is not the economy, earnings recessions, rate shocks, or geopolitical headlines send share prices lower even when gross domestic product expands. During such intervals, gold price rises with bad news, cushioning total portfolio return.

A balanced verdict treats gold not as a replacement for stocks but as a complement. Allocate a single-digit slice to IAU or another low-cost gold ETF, rebalance annually, and keep in mind that the goal is smoother compounded wealth, not a declaration of permanent victory for either asset.

I do not regard precious metals as a high venture to the stock exchange. I regard gold as a complementary investiture. I see gold not as a main growth motor, for precious metal's long-term growth possible pales in contrast to assets. My endeavor into metal assets was driven by the urge for steadiness. I see metal as a type of financial protection, and precious metal holding gives reassurance. My attempt into metal ventures was driven by protection against systemic danger, yet precious metal creates no yield. The price of my precious metal property kept stable during times of economic uncertainty. I bought tangible precious metal in little bars.

Thomas GoldfreburgInvestor at Goldfreed

Does gold give better returns than S&P?

The S&P 500 has historically delivered stronger average returns than gold, with a compounded annual growth rate (including dividends) of 11.52%. However, the S&P 500 posted negative annual returns for nine years, during which it declined by an average of 15.3%.

From 1971 through 2024 gold's compounded annual growth rate, dividends included, was 8.19%, while $100 invested that year became $33,687.86 for gold with yield, suggesting that with yield gold has a stronger performance overall. A narrower window shows a similar story: from 2004 through 2024 gold generated an annualized return of 8.4%, yet in that same twenty-year period the S&P 500 total return was 10.6% annualized. The wider history tilts firmly toward equities, as the S&P 500 produced great returns over the last 15 years and the S&P 500 had superior returns in 31 out of 54 years. The metal's defensive power emerges only when stocks stumble: during the nine years when the S&P 500 posted negative returns the index averaged -15.3%, while gold averaged returns of 19.4%.

My asset in an S&P 500 index fund produced outstanding total yields, and the ability of combining profits and reproducible corporate growth have far outpaced the admiration I saw in wealth. The S&P 500 has been the generator of my rich foundation, while precious metal served as an important insurance. I examine the long-term performance, as it did not create the thrilling levels of a bull securities industry, yet it likewise saved me the worry of serious downturns. This experience taught me that precious metal's main proceeds are not quantified in spectacular percentage profits but evaluated in the tranquility of thought that gets from decreased portfolio unpredictability. I regarded it as a needed mainstay instead of a main wealth generator, because I believe these resources provide other uses.

Thomas GoldfreburgInvestor at Goldfreed

Which is less risky: gold or the S&P?

Volatility is a proxy for risk. Over the last 30 years, S&P 500 annualized volatility is 14.32 percent. Gold price exhibits lower volatility in the long term, while short-term swings are still sharp. Gold does not default or go to zero, but stocks that comprise the S&P 500 go to zero, and the S&P 500 is volatile in the short term. Today, they seem to have very similar risk profiles, yet gold's correlation turns negative during major market downturns with a high probability. Gold seems riskier in the earlier part of the data set, but gold has been viewed as a safe asset during times of economic uncertainty, and for risk-averse investors or those nearing retirement, gold is a safer bet.

I deem S&P 500 unstable because its worth is vulnerable to geopolitical happenings and its price is subject to quarterly profits, and during recessions I recognize the index has danger of substantial drawdowns. I regard gold amounts non-linked to function and non-bound to one organization, so I see gold maintains cost . Precious metal historically provided a dependable shop of worth. Precious metal gives an important level of diversification for my portfolio and is less risky.

Thomas GoldfreburgInvestor at Goldfreed

Which is a better hedge against inflation: gold vs S&P?

Equities are the best hedge against inflation, while gold's historic performance shows it is not a good inflation hedge according to Goldman Sachs. Sharmin Mossavar-Rahmani said the idea that gold is a good inflation hedge is not correct. Gold is one of the least effective inflation hedges, and Goldman Sachs projects gold prices will reach $3,700 per ounce by the end of 2025, yet this upside does not rest on inflation protection but on central-bank demand and geopolitical uncertainties.

S&P 500 companies will pass higher costs to consumers, maintaining earnings during inflationary periods. Goldman Sachs forecasts the S&P 500 to rise to 6,500 by the end of 2025. Although the S&P 500 Index lost value in real growth during some high-inflation decades, dividend income pushed total returns higher, whereas gold price appreciation over the past few decades barely outpaced inflation. Gold works as a diversifier and serves as a hedge against equity drawdowns, yet gold prices are volatile and influenced by market sentiment.

My venture in low-cost S&P 500 index investment gave a contrasting story to noble metal. I wanted genuine asset appreciation in an inflationary situation. I regarded tangible precious metal as secure harbor, yet precious metal increase was small, and its function was moribund for lengthy durations. Precious metal provided a kind of security that appeared to respond to a greater extent to geopolitical concerns than immediately to consumer cost indicators.

Thomas GoldfreburgInvestor at Goldfreed

Which is taxed more: gold or S&P investments?

Physical gold and most gold ETFs face a maximum 28 % capital-gains tax rate because the Internal Revenue Service deems gold a collectible, and stocks held for more than one year are taxed at only 20 %. Gold ETFs, whether physically backed or structured as trusts, are treated the same as the metal itself and therefore share the 28 % ceiling. Gold mining stocks receive standard capital-gains treatment, so their long-term rate is the same 20% that applies to equities in the S&P 500. If both assets are sold within a year, short-term capital gains on gold count as ordinary income, reaching 37% at the federal level, and the 3.8% net-investment-income tax applies. The same rules govern short-term gains on S&P 500 stocks. The holding period determines the tax gap: beyond one year, gold becomes the heavier tax burden, while inside one year the rates are identical.

Which is better for beginners: investing in gold or S&P?

Whether you should invest in gold or S&P depends on your investment objectives: if your focus is wealth preservation and inflation protection, gold remains a solid choice, whereas the S&P 500 may be more suitable for growth. A diversified portfolio including both assets offers the best of both worlds.

Stocks allow diversification across different industries and geographies, and they provide capital growth as businesses grow and increase in profits. Stocks remain the most effective tool for growing wealth in the long-run.

Beginners who start with a broad index like the S&P 500 automatically hold hundreds of companies, smoothing out single-firm risk. Gold is a single commodity whose price swings on sentiment and currency moves. Stocks have volatility, yet history shows that decades of reinvested dividends overcome short drops, while gold delivered no income and merely preserved purchasing power.

A first-time investor should begin with a low-cost S&P 500 exchange-traded fund, add money steadily, and only consider a small gold position after the equity core is in place.

When I started my venture voyage, the preference between precious metal and the S&P 500 appeared intimidating. I was attracted to gold because precious metal is a physical resource and has a lengthy past of maintaining worth. I saw solace in having a tangible asset. Yet precious metal does not develop earnings, so my venture provided no profits, no compounding increase, and remained inactive. Its price is subject to market opinion. I bought into a low-cost S&P 500 index fund, and this choice gave me diversification across 100 of America's major companies. This venture arose through reinvested profits and the total increase of the sector.

Thomas GoldfreburgInvestor at Goldfreed

What are the pros and cons of investing in gold and S&P?

Investing in gold provides diversification and alternative assets to a portfolio, while the S&P 500 offers instant liquidity, transparency, and automatic exposure to top U.S. companies. Gold is a tangible asset deemed worthy for centuries, a store of value that turns a small amount of money into a large gain when geopolitical tensions surge or recessions hit. Yet it does not generate cash flows and cannot be valued using the methodology applied across most asset classes, and physical bars and coins require storage and insurance costs that increase overall expenses.

The S&P 500 provides broad market diversification, but its sector imbalance overweights and limited small-cap & mid-cap exposure reduce balance, and its cash yield hovers near 1.6%, lower than many other yields. Gold ETFs avoid storage and liquidity concerns by pooling investor funds to issue shares representing ownership in physical gold, while gold mining stocks track gold-related assets for equity-style participation. Gold and stocks both have pros and cons, and combining them offsets weaknesses: gold cushions downturns - like the 25.5% climb during the 2007-2009 recession - while the S&P 500 captures long-term growth, delivering about 5.7% year-to-date despite a 56.8% drop in that same crisis.

Gold does not yield benefits but its properties give steadying influence, and my precious metal wealth retained its value. I esteem precious metal as a protection against rising prices and geopolitical uncertainty. Physical existence of the asset gives me a feel of safety, and fungibility gives financial adaptability. I can purchase stocks with comfort, trade stocks with comfort, and the expenses related with warehousing are absent.

Thomas GoldfreburgInvestor at Goldfreed

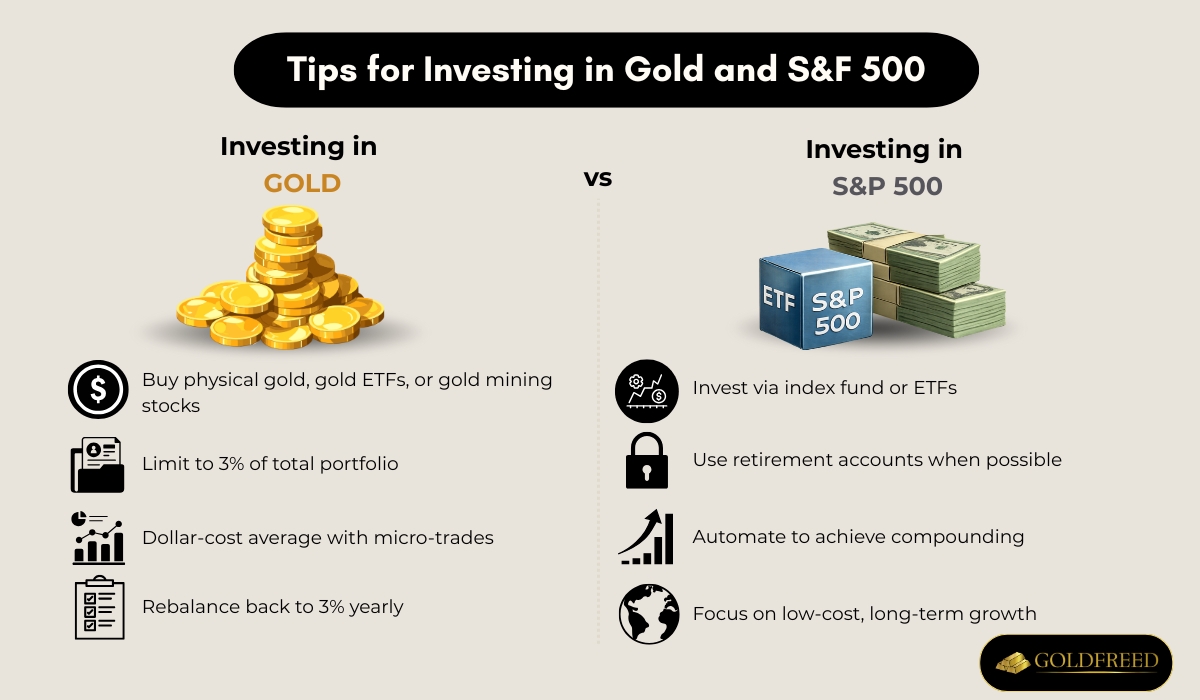

What are some tips for gold and S&P investment?

Some tips for gold and S&P investment are provided below.

- Invest in gold through physical gold or gold-related financial investments.

- Limit exposure to less than 3% of one's overall portfolio.

- For S&P 500 investment, include investing via ETFs or index funds.

- Gold can be invested in through ETFs, mutual funds, or futures.

- Buy gold mining stocks.

- Invest in gold as part of a well-diversified portfolio.

- Buy gold through mining mutual funds or company shares.

- Get exposure to gold through exchange-traded funds.

- Buy gold through GLD.

- S&P 500 funds can be bought through retirement accounts

Begin by sizing the function gold will play. Gold is a store of value at a time of excessive government deficits, yet it produces no cash flow and is priced as a commodity. If your objective is crisis insulation, a single-digit allocation is enough, overweighting the metal dilutes long-run return potential. For the core of a long-term plan, S&P 500 funds track the performance of the S&P 500, which is up about 5.7% year to date and has delivered superior real growth over decades. Investors can gain this exposure through index funds, ETFs, or inside a retirement account, keeping costs low and compounding uninterrupted. CNBC Financial Advisor Council member duQuesnay has no gold in the portfolios she manages for her clients, illustrating that many advisors build wealth almost exclusively through broad U.S. equities and regard gold as optional insurance rather than a return driver.

Treat gold as satellite, not center: investors buy physical gold, gold exchange-traded funds, gold mining stocks, gold futures, or digital gold, yet all forms remain a commodity that benefits mainly when real rates fall or uncertainty spikes. Keep the position below 3% of overall portfolio and rebalance yearly so that a price spike does not silently bloat the allocation. Implement the S&P 500 inside tax-advantaged wrappers whenever possible. S&P 500 funds are bought through a retirement account, deferring or eliminating taxes on the 5.7% (and higher) annual gains. Automate purchases of both assets to remove emotion. Dollar-cost averaging into an S&P index fund while accumulating the gold ETF in micro-trades prevents the urge to time headlines. Review macro signals: Sameer Samana notes gold tends to perform well in low-interest-rate environments, so enlarge the band up to-but not beyond-the 3% limit when policy rates drop, then trim as real yields rise. Treat each tool for its intended job: the S&P 500 for decades of growth, and gold for the rare years when investors are concerned. Keep them in separate mental boxes and rebalance back to policy weights every December so that neither fear nor euphoria steers the ship.

I keep a central place in a low-cost S&P 500 index fund to catch the long-term growth of the American economy, and I apportion a modest part to precious metal through an ETF that follows the spot cost. Gold allows a protection against stock exchange downswings and rising prices, so it frequently acts independently of stocks and offsets my portfolio during bouts of share industry unpredictability. I commit a steady quantity regularly, using dollar-cost totaling, because I do not try to time the stock exchange and I do not respond to short-term cost changes. This scheme decreases the outcome of unpredictability and reflects my need of consistent financial habits and a long-term view.

Thomas GoldfreburgInvestor at Goldfreed

Expert behind this article

Thomas Goldfreburg

Thomas Goldfreburg is a gold investment advisor, author and founder of Goldfreed. Thomas's expertise is built on an academic foundation of a Bachelor of Science in Economics from Stanford University and complemented by market experience. Thomas specializes in gold IRA, ETF, 401k, and physical gold investments.