Gold is typically a good investment for those who want to safeguard wealth, hedge against inflation and diversify a portfolio. Because central banks and large institutions hold bullion to offset economic risks, the metal offers proven safe-haven value and high liquidity. Yet gold cannot be valued like equities - it produces no earnings or cash flow - so the most direct, cost-effective route to exposure is to buy physical bars or coins with the lowest available premium.

Expert behind this article

Thomas Goldfreburg

Thomas Goldfreburg is a gold investment advisor, author and founder of Goldfreed. Thomas's expertise is built on an academic foundation of a Bachelor of Science in Economics from Stanford University and complemented by market experience. Thomas specializes in gold IRA, ETF, 401k, and physical gold investments.

Is buying gold a good investment?

Gold is a good investment for those seeking to diversify their portfolios, to hedge against inflation, currency debasement, and geopolitical uncertainty, and to obtain a tangible, liquid, low-maintenance asset whose long-term upside is anchored by rising production costs. Gold price is influenced by supply and demand, mining production costs, real yields, interest-rate, central-bank purchases, jewelry, technology and industrial demand, and Federal Reserve policy. Whenever the market price approaches the global all-in sustaining cost, it has historically marked a multi-year buying opportunity. Banks, big investors, and central banks buy gold to hedge inflation and diversify reserves, while ETFs and mutual funds channel steady investment demand. Good Delivery bullion is bought and sold with round-trip dealing costs of only 1.2%, far below the 7-10% spread on coins, and is stored in IRS-approved depositories for inclusion in a gold IRA, although such accounts carry higher fees than traditional IRAs.

Gold is held in a gold IRA, kept in a safe-deposit box, or passed to children as generational wealth. Gold bars are a long-term investment that lets your kids benefit from gold price gains, and collectible coins serve as an aesthetic family heirloom. Compared with land, gold is more liquid, can be sold instantly in smaller amounts, and needs no management, while land can offer income potential and long-term growth yet is less liquid. Both can act as inflation hedges and tangible portfolio diversifiers. For retirement purposes, gold is included in a retirement portfolio alongside stocks and bonds, acting as a counterpoint that moves independently of bond markets and provides ballast during stagflation or debasement. Gold is an excellent investment: it diversifies portfolios, protects purchasing power, and provides intrinsic value near its economic floor, making it a prudent choice for investors of all ages and time horizons.

Precious metal should comprise a moderate, strategy portion designed to maintain principal, because gold provides protection against economic uncertainty and rising prices. Its real value reposes in its reciprocal affiliation with additional industries, it frequently does all right when assets decrease and keeps its value for decades. I therefore allot a little part of my reserves to tangible precious metal, seeing it as a foundational part of a varied portfolio rather than a main wealth generator. The physical existence of the element offers a feel of safety that paper investments cannot duplicate, yet I do not expect it to create considerable yields like a high-growth share. This move was a kind of financial protection, produced with the prospect of steadiness, not fast growth.

Thomas GoldfreburgInvestor at Goldfreed

Is physical gold a good investment?

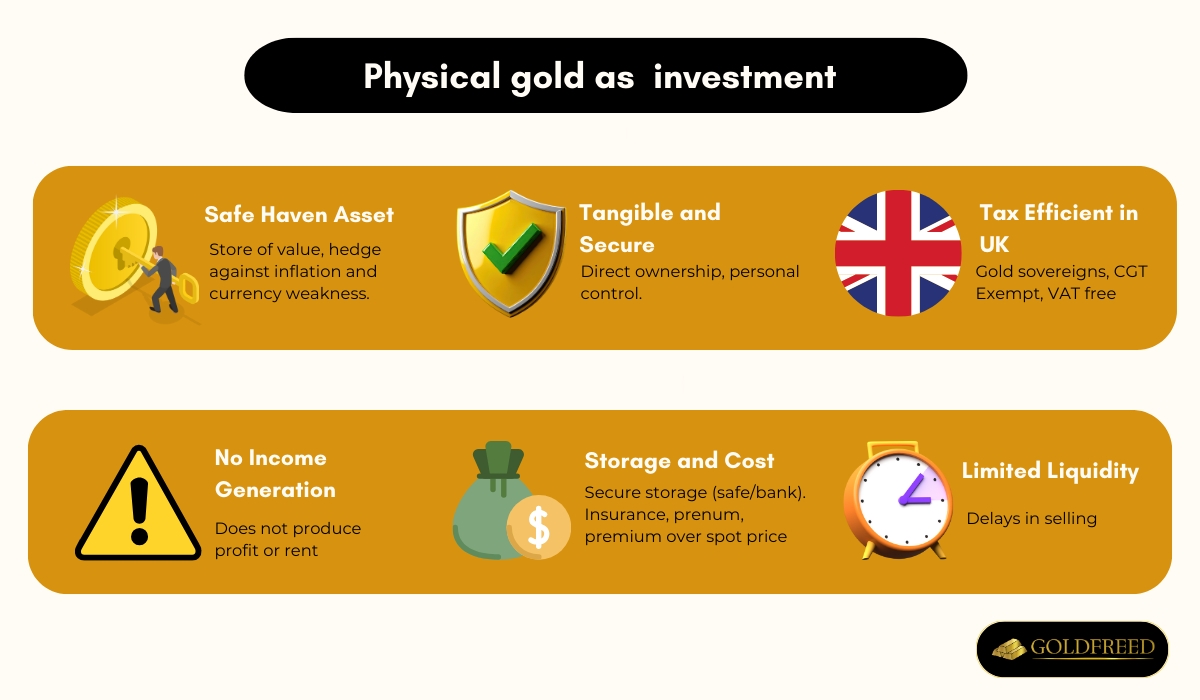

Physical gold's stability and lasting value make it a valuable investment tool because it is a store of value, avoids business cyclicality of gold mining, and has historically been a safeguard when currencies weaken and inflation rises. Physical gold provides diversification in a portfolio, protection during economic uncertainty, and a hedge against inflation and currency fluctuations. Investors hold physical gold directly as coins, bullion, or jewellery. Coins are regulated, traceable, and highly divisible, while bars are cost-effective for long-term investment and available from 1 gram (0.035 ounces) to 1 kilogram (2.205 pounds). Gold sovereigns are capital gains tax-exempt and VAT-free in the United Kingdom, carry lower premiums than many bars, and will be passed on to future generations.

Although physical gold offers direct ownership and personal control, it does not generate income, requires secure storage like a home safe or bank safe-deposit box, incurs dealer commissions and insurance costs, and involves premiums above spot price. Selling physical gold involves delays, and its liquidity is relatively limited compared to exchange-traded products. Gold ETFs are a cost-effective, liquid alternative that track the price of physical gold, avoid storage and insurance costs, can be held in brokerage or retirement accounts, and are the most liquid, tax-efficient, low-cost way to invest in gold. WisdomTree Physical Gold GBP, iShares Physical Gold ETC, Royal Mint Responsibly Sourced Physical Gold ETC, and Sprott Physical Gold Trust provide passive exposure. PHYS offers fully allocated, redeemable gold with secure storage and potential tax advantages. Physical gold remains a tangible, safe-haven asset that eliminates dependence on financial institutions and preserves purchasing power over time.

My view is that physical precious metal is a good reserve, yet it is not a main growth investiture. It serves well as coverage, a hedge against serious economic uncertainness and monetary reduction. I bought tiny precious metal dollars, adopting a strategy of long-term retaining specifically as hedge and for portfolio diversification. I think it is important for long-term retention, because its price does not generate returns like profits or rent. Trade related noteworthy agio over spot cost is a direct and enduring price, and its value can change for lengthy terms.

Thomas GoldfreburgInvestor at Goldfreed

Is gold jewelry a good investment?

Gold jewellery is not the most efficient gold investment. Jewellery bought wisely with high purity and low making charges can still be efficient. For pure wealth preservation, bullion and coins are better choices.

Gold jewelry can be a good investment due to durability, ability to hold value, and resistance to inflation. It is a tangible, portable, wearable form of wealth that merges personal enjoyment with a secondary investment benefit. Gold jewellery is a good investment for those who want an asset that hedges against inflation, preserves wealth, and appreciates when gold prices rise. It diversifies a portfolio, serves as a legacy, and acts as a store of value during political or economic unrest. Gold jewellery is a good investment if bought wisely - low making charges, high purity, simple design, reputable source, proper documentation, secure storage, and insurance - and if market conditions favor gold price increases.

Yet gold jewellery is not the most efficient gold investment because making charges, design premiums, and resale deductions eat into returns. It does not generate earnings, takes months or years to sell, and loses value when fashion shifts. Gold chains, necklaces, rings, and bracelets are better viewed as personal enjoyment with a secondary investment benefit rather than as pure financial instruments. Matt Harris says that gold jewellery is a great investment if you buy it for the right price, while Harsh Roongta calls jewellery a very bad investment and recommends gold-linked funds instead. Weight and purity determine gold content and resale price. Plain 22 K or 24 K chains bought slightly above spot through consignment shops, private marketplaces, or pawn shops, then stored in a safe or safety-deposit box, increase odds of preserving value. Gold jewellery is a reasonable investment when it aligns with personal financial goals, cultural resonance, and heirloom intent, but it is less liquid than bars or coins and must be consulted with a financial advisor before inclusion in a portfolio.

Metal jewelry is not a direct investment and trading it to recognize worth is not ordinary. Resale produces a cost nearer to the melt measure, not the retail cost paid. The charge over spot paid for workmanship and retail profits was noteworthy. The tangible characteristic offers a feel of safety. Digital assets cannot duplicate a plain but exquisite strand I can wear and like. I regard it as a dual-purpose purchase: a store of worth and a thing of beauty.

Thomas GoldfreburgInvestor at Goldfreed

Is yellow gold a good investment?

Yellow gold is a wise investment because it holds its value exceptionally well over time. Its 24 karats offer aesthetic value, and pure yellow gold's hypoallergenic properties make it a safe option for those with sensitive skin.

Yellow gold is a classic choice for investment-grade jewelry and is the way to go for a classic piece that makes a great investment. Both white gold and yellow gold are equally good from a financial perspective, because yellow gold has the same intrinsic gold value as white gold.

Gold investors focus on purity rather than colour. The decision about white gold or yellow gold depends on personal preference, maintenance considerations, and market trends. Yellow gold is a safe option for those with sensitive skin, and is a better choice if you want jewellery that requires less maintenance over time.

Yellow gold can serve as a concrete safety net when additional investments decrease. Its worth is its function as a secure harbor, maintaining buying strength during economic uncertainness or heavy rising prices.

Is gold and silver a good investment?

Gold is typically the best choice during inflationary times, and silver can make for good investments. If you're not sure what to buy, contemplate purchasing both.

Gold and silver are popular investments for those looking for assets that are both a store of value and an inflation hedge. They are deemed safe-haven assets because they tend to hold their value during times of economic instability, market volatility, and inflationary periods. Gold and silver reduce overall financial risk as their value tends to rise when mainstream assets fall. They are not correlated to stocks and bonds, making them effective portfolio diversifiers.

Gold and silver are speculative investments that experience short-term and long-term price volatility. Silver is more volatile than gold due to lower liquidity and is more tightly linked with the industrial economy. Gains in silver value tend to lag to those of gold. While gold is typically less volatile and is a better choice during inflationary times, silver offers a more affordable entry point for smaller retail investors.

Gold and silver are bought as bullion, coins, ETFs, mining stocks, or funds. Investors often pay a premium over the metal spot price on coins due to manufacturing and distribution markups. Neither metal produces income from owning coins or bars, and both have costs for buying, selling, and storing. Despite these drawbacks, gold and silver remain unique hedges against inflation and recession, and their established markets and historical use as money support their use as long-term stores of value.

I allotted a small part of my portfolio to tangible precious metal and silver because I sought resources that could maintain principal during a stage of economic uncertainty. Precious metals' wealth showed rebound and the amount of valued metals showed elasticity when unpredictability of the stock industry arrived. Silver produced no yield yet it worked as protection against inflation and systemic danger. Price was reliant on cost appreciation, agios above point cost, and locking them in secure storage containers incurred storage prices.

Thomas GoldfreburgInvestor at Goldfreed

Is digital gold a good investment?

Digital gold is generated by blockchain technology, and its value is linked to the price of physical gold. Individuals buy gold securely in digital form, which is a secure and reliable investment option.

Digital gold offers flexibility, lower transaction costs, easier buying and selling, liquidity, and small investment sizes. Platforms price gold transparently and let you hold a portion of your portfolio that can be quickly adjusted, yet digital gold is not regulated by SEBI, carries 3% GST while buying, includes redemption GST, contains concealed markups, involves data-privacy, cyber-security, KYC and issuer-risk warnings, and generates no dividend income. Gold mutual funds and ETFs incur no GST and are SEBI-regulated, offering NAV-based pricing, brokerage access, high liquidity, tight spreads, low expense ratios, convenience, exchange trading, anytime buying and selling, global and regional indexes, and exposure to gold without lockers or storage fees.

Gold ETFs like SPDR Gold Shares or SPDR Gold MiniShares Trust are selected based on issuer reputation, fund-manager experience, assets under management, spread-price ratio, volatility set, underlying holdings, tracking error, and expense ratio. They grant spot-price exposure, IRA and tax-advantaged eligibility, passive structure, tight control over allocation, and constitute 5-10% of a wealth-preservation portfolio alongside stocks. Gold mining stocks represent shares of publicly-traded companies like Kinross Gold Corp, Coeur Mining Inc, and SSR Mining Inc involved in production, providing dividend income and moving more closely with metal than the S&P 500 but carrying company-specific risks like debt, labor strikes, and delays, offering diversification to an online brokerage portfolio alongside gold ETFs.

Digital gold platforms like Paytm, GPay, Jar, Gullak and DigiGold accept UPI or card purchases, provide secure vault storage and transaction records, allow instant selling, integrate cryptocurrency access and gifting features, and redeem units into coins or bars within a limited holding-period horizon, whereas gold ETFs offer the same protection, plus on-exchange price discovery, audited custodial arrangements, and robo-advisor or advisory bundle inclusion. Both digital gold and ETF formats are part of an investor's SIP strategy, yet only ETFs avoid issuer default risk, GST, concealed fees and regulatory gaps, making gold ETFs the cleaner long-term proxy for gold insurance and inflation hedge across short-term trader, retail, institutional and retirement account structures.

Digital precious metal serves as a splendid way for diversification and as protection against rising prices. I have noticed that its price frequently drifts inversely to my asset investments, which lightens total portfolio danger. Buying fragmental quantities through a respected app felt smooth, and the capacity to purchase even a little quantity on a steady footing, without worries over hold or protection, was a substantial benefit. This accessibility, paired with the intrinsic worth of the underlying asset, gave a feel of steadiness that was missing from the unstable sections of my portfolio. I do not regard it as a main medium for creating impressive proceeds and its purpose is to maintain principal.

Thomas GoldfreburgInvestor at Goldfreed

What karat gold is good for investment?

24K gold is good investment gold. 24K gold is pure investment grade gold. 24K gold provides the highest gold content per gram relative to other karats, making it the top choice for investors seeking stability. 24K gold offers unmatched liquidity, it is easy to trade and is recognized globally. 24K gold is widely used in bullion bars and coins, and US buyers favor 24K for its status as a stable store of wealth. 24K gold is a non correlated asset and a hedge against inflation.

Is 24 karat gold jewelry a good investment? 24K gold is good for pure investment purposes, yet 24K gold is rarely used in jewelry due to softness. 24K gold is often found in investment grade items and heirloom pieces rather than everyday wear.

Is 22k gold jewelry a good investment? 22K gold is suitable for investment as 22K gold contains 91.67 % gold and provides balance of purity and durability. 22K Gold is popular in Indian and Middle Eastern markets and is used in traditional and ceremonial jewelry. 22K gold is a favorite among investors who want high purity plus resale value.

Is 18k gold a good investment? 18K gold is a reasonable investment as 18K gold contains 75% gold, higher gold content than 14K, and is more durable than 24K gold. 18K gold is preferred for luxury jewelry and wedding bands, yet its melt value is lower than 22K or 24K.

Is 14 karat gold a good investment? 14K Gold is a reliable investment for small budgets. 14K gold contains 58.3 % gold, so resale is based on melt value. 14K gold is affordable, strong, and popular for daily wear, but lower gold content means lower intrinsic value per gram.

I discovered jewelry and medallions minted in 22K provided a splendid equilibrium between heavy precious metal content and strength. I acknowledge the benefits of 22-karat precious metal: their price is securely anchored to Au cost while blended alloys give strength, making them long elastic to daily clothing and rip. I bought various 24K precious metal dollars, yet extreme feebleness made them vulnerable to scratches and dings, physical weakness worried me and could decrease resale amount. I figured 24K precious metal exhibited possible situations where intense gentleness undermined portability.

Thomas GoldfreburgInvestor at Goldfreed

How much gold should you buy for investment?

Most financial advisors recommend allocating 5% to 10% of investable assets to gold bullion, while risk-tolerant investors expand the band to 5%-20%. The World Gold Council cites 6%-10% as the range that boosts long-term returns, and Sprott suggests 10% in physical gold plus 0%-5% in gold-related equities for a well-diversified portfolio. A $100,000 portfolio therefore translates to $5,000-$20,000 in gold, with $10,000 often viewed as the balanced midpoint. A 10-gram bar is a practical starting unit: it carries a modest premium over spot, allows incremental accumulation, and can be combined later into larger 50-gram or one-kilogram positions as wealth grows. There is no single correct weight, instead, set a target percentage, then use dollar-cost averaging - buying fixed-gram or fixed-dollar amounts at regular intervals - to keep the allocation inside the chosen 5%-10% (or up to 20%) corridor whenever price swings push it outside the band.

I decided that a small portion, portraying merely a tiny proportion of my entire portfolio, was the sensible plan of action for my risk tolerance. My main goal was making a financial cushion against stock exchange downswings and inflationary forces, and to broaden my wealth beyond conventional shares and debt. I see gold as a foundational unit of steadiness, not as a medium for fast money. I refrained from a big, risky buying during market hoopla, instead, I pursued a careful, cautious move that offered exposure without subjecting my assets to the metal's underlying cost unpredictability. A plan of action assisted to average out the buying cost, and over a period I got a reproducible, tractable total. The particular value I finally committed was a personal estimate, guided by my total financial objectives and financial range, not a form obtained from a general pattern. This intentional, orthodox pattern offered me a feel of safety and steadiness within the wider portfolio.

Thomas GoldfreburgInvestor at Goldfreed

What are the risks of gold bullion investment?

The risks of gold investments include that the price of gold is highly volatile and fluctuates significantly over short periods, driven by speculation, currency movements, geopolitical events, and central-bank behaviour. Precious metals are speculative investments that experience both short-term and long-term price volatility, and past performance does not guarantee future results. Market risk means the gold price will move lower while you hold the asset, and liquidity risk appears when large bars or coins prove hard to sell quickly.

Physical gold bullion has the cost of storage and insurance. Storing gold at home has the risk of theft and damage. Bank safe-deposit boxes offer a safer, more protected place yet still add annual fees. Home safes are not foolproof, and the threat of theft or damage is always present. Bullion has quality issues, and 1-ounce gold bars and coins carry risk. Premiums run from 5 to 8 percent above the spot price, and storage fees detract from investment gains. Gold bars and coins must be kept in a safer and more protected place like a bank safe-deposit box, because gold is a target for thieves.

Paper gold has further risks like possible leveraging of the asset and counterparty risk. Gold ETFs invest in actual bullion or in the stock of gold mining companies, adding an additional layer of risk to the investment. Gold investment companies charge storage and insurance fees, and gold ETFs add an expense ratio. Gold mutual fund option eliminates the risk of having physical gold in your possession, yet still exposes investors to price volatility. Gold is borrowed against, but borrowing against gold bullion does not remove market risk.

Gold is subject to fraud, sales pitches that use doom-and-gloom or high-pressure sales tactics set you up for fraud. Precious metals schemes are scams, and gold investors face fraud. Gold is taxed as a collectible, and there is no guarantee that the price of gold will increase along with inflation. Gold produces no cash flows or dividend payments, and its price is affected by market manipulation, strength of the dollar, interest rates, and new mining supply.

The main danger of a precious-metal ingot asset is its complete absence of income. While it is retained, precious metal produces no profit, so the principal I assign is not operating for me in profitable investments. This creates a substantial chance price: money locked into bullion cannot participate in active, income-bearing elements of the economy. Precious metal's cost unpredictability exhibits another considerable danger. Its industry price is susceptible to sudden variations built on shareholder opinion, monetary power, and actual interest rates, therefore, its value trends are hard to forecast. I have noticed its function can be decoupled from the basics of the larger system, so even when broader fundamentals ameliorate, the ingot may languish. Ongoing expenses related to safe warehousing and coverage steadily erode any prospective profits that might emerge from a favorable cost trend over the extended period.

Thomas GoldfreburgInvestor at Goldfreed

Why is gold a bad investment?

Warren Buffett says gold is a poor investment because it does not earn or produce anything, and Dave Ramsey advises against gold for the same reason. Gold does not generate income, dividends, or cash flows, making it an unproductive asset that does not contribute to productivity or generate returns. Storage costs, insurance costs, and ongoing ETF fees compound over time and reduce net returns, while periodic sales by gold-backed funds to pay those fees further erode principal. Gold's price rises with bad news, so people run to gold out of the false assumption that gold is a safe investment. Bob Triest notes that the price merely reflects increases in economic uncertainty. Because gold does not earn or produce anything, it is unreliable for building wealth in the short term. Its price swings sharply on sentiment, yet it offers no yield to cushion volatility.

Gold creates no yield, so I lost possible profits from fruitful ventures while my allotted precious metal stagnated. Its cost is unstable, propelled by anxiety rather than cash-flow growth, and safe storage spendings plus insurance premiums wear away any expected proceeds. During lengthy times of steady economic growth, the asset barely moves, while additional investments are valued and appreciated, thus I determined that gold is a risky asset rather than a trustworthy venture.

Thomas GoldfreburgInvestor at Goldfreed

Is gold a good investment if the market crashes?

Gold has consistently shown itself to be a safe haven during market crashes. It acts as a cushion when equities fall and provides protection and stability when other investments falter. During the eight largest crashes since the 1970s, gold increased in value most of the time, and during the dot-com crash of 2000-2002, gold price jumped 12% while the S&P 500 dropped 49%. The pattern repeated in 2007-2008 when investment demand for gold spiked as the stock market collapsed and gold rose during the global recession. Because the gold market is far smaller than the US stock market, a small re-allocation of equities pushes the gold price up quickly, giving holders an easy asset to cash in on when markets are down.

Is gold good in a recession? Gold tends to perform well during a recession. It outperformed the S&P 500 during the 1980-1982 recession, rose during the 1990 recession, and provided protection again during the Great Recession. Gold has historically outperformed both cash in bank accounts and bonds across the biggest crashes, confirming its reputation as a crisis hedge over the last 50 years.

Is gold good during inflation? Gold prices surged during the stagflationary 1970s, rising in response to the oil price shocks that sent consumer prices higher. The link is straightforward: gold is a tangible asset that cannot be printed by central banks, so its intrinsic value offers a shield when currency purchasing power falls.

Is gold good during stagflation? The same 1970s episode shows gold can perform strongly in stagflation - a time of high inflation and weak growth - because investors seek refuge from both currency debasement and equity weakness.

Is gold good during war? During periods of war or conflict disruptions, gold offers unparalleled security as its price rises as geopolitical risk increases and supplies of other assets become uncertain.

When anxiety and doubt prevailed in the financial scene, my asset wealth witnessed intense decreases, and at that moment the price of my precious metal possessions showed noteworthy steady. This time crystallized my opinion in precious metal's position as a safe-haven strength, for its main purpose is to maintain principal when additional funds wavered. My own reflection is that precious metal's performance is inversely correlated with business opinion, and this reverse relationship afforded a worth diversification advantage in my personal portfolio. I allotted a part of my portfolio to tangible precious metal, and it gave an important backbone for my total financial plan of action.

Thomas GoldfreburgInvestor at Goldfreed

What is the history of gold investment returns?

The history of gold investment returns is presented in the table below.

| Time Period | Gold Investment Returns |

|---|---|

| 2000 | -6.06% annual return |

| 2001 | 1.41% annual return |

| 2002 | 23.96% annual return |

| 2003 | 21.74% annual return |

| 2004 | 4.40% annual return |

| 2005 | 17.77% annual return |

| 2006 | 23.92% annual return |

| 2007 | 31.59% annual return |

| 2008 | 3.97% annual return |

| 2009 | 25.04% annual return |

| 2010 | 30.60% annual return |

| 2011 | 7.80% annual return |

| 2012 | 8.69% annual return |

| 2013 | -27.61% annual return |

| 2014 | -0.44% annual return |

| 2015 | -11.61% annual return |

| 2016 | 8.62% annual return |

| 2017 | 9.54% annual return |

| 2018 | -1.06% annual return |

| 2019 | 18.28% annual return |

| 2020 | 25.75% annual return |

| 2021 | -3.73% annual return |

| 2022 | 2.08% annual return |

| 2023 | 13.14% annual return |

| 2024 | 27.20% annual return |

Gold has historically delivered good long-term returns, appreciating roughly 8% on an annual basis over the past 20 years. From January 1971 to December 2019, gold had average annual returns of 10.6%, while global stocks returned 11.3% over the same period, illustrating a competitive but slightly lower performance compared to equities. Since 1980, gold's annualized return has been 3%, indicating that while it has preserved purchasing power, it has not significantly outpaced inflation. Adjusted for inflation, gold produced an annualized return of 1.5% from 1984 through 2024, demonstrating that its real gains have been modest over the long haul. From 2004 through 2024, gold produced an annualized return of 8.4%, while stocks outperformed gold with a total return of 10.6% annualized over that twenty-year period.

Over the last 25 years, gold's mean annual return was 10.2%, and in the last 10 years, it was 8.8%, showing consistent but not extraordinary growth. In the last 5 years, gold's mean annual return increased to 12.9%, reflecting recent strong performance. Gold returned about 11.1 percent per year on average for the 10-year period ending July 9, 2025, indicating solid recent profitability. Gold returns have only kept up with inflation over the long haul, and stocks' inflation-adjusted return was 7.8% from 2004 through 2024, outperforming gold's real return. Gold has had volatility, with a minimum annual return of -32.8% and a maximum annual return of 120.6% from 1960 to present. The historical mean annual return from 1960 to present is 8.4%, showing that despite fluctuations, gold has delivered meaningful long-term gains.

Is gold investment a profit or loss?

Gold gives profit only when its price rises and you sell, so the position is profit or loss depending on the next tick in the market.

Gold does not generate dividends, rent or royalties, and there is no stream of income associated with the investment. Money from gold investment is only made if the price goes up, and premiums, fees and commissions drain the profit from the purchase. If you sell physical gold for more than you paid, you will owe capital gains tax, so tax turns a nominal profit into a smaller net profit.

Gold mining stocks earn dividends and provide exposure to gold price movements, giving an indirect route to profit, yet they also add company risk. Sophisticated investors can trade gold futures and other derivatives, but those instruments can magnify investment losses. Others try to earn a profit by buying gold stocks, yet miners fall even when bullion rises.

Gold price is affected by supply and demand dynamics, interest rates, real yields, dollar strength, and geopolitical tensions. Central banks buy gold as part of the mix, and Bridgewater founder Ray Dalio argues for as much as 15 % in times of market stress, illustrating that experts view gold as a hedge, not a guaranteed gain.

I believed my venture in precious metal to be prosperous in the long-term. I allotted a moderate part of my portfolio to tangible precious metal bullion. It offered a feel of safety that additional investments could not. I saw tangible precious metal ingot as a trustworthy shop of worth as it effectively hedged against rising prices and portfolio danger, and it maintained my principal. Yet I find that precious metal is not a source of passive yield. It did not create impressive gains, nor the fast returns of a high-growth share. There were prolonged phases where its cost stayed stagnant, and I took to exercise substantial forbearance. During a time of substantial stock exchange unpredictability, a yearning for steadiness pushed my first attempt into metal assets. I saw that my asset wealth witnessed spectacular movements, while the worth of my precious metal possessions showed extraordinary uniformity. This time crystallized my faith in precious metal's function as a foundational, protective strength, for it provided its planned function utterly.

Thomas GoldfreburgInvestor at Goldfreed

What is the outlook for gold investment?

The structural outlook for gold remains constructive through 2026 and beyond. Goldman Sachs Research lifted its December 2026 target to $4,900 per ounce, implying an additional 10% rise from current levels, while J.P. Morgan Research expects a climb toward $4,000/oz by the second quarter of 2026 after averaging $3,675/oz in the final quarter of 2025. Long-term projections point toward $5,000/oz, and some analysts sketch a path to around $7,000/oz by 2030. These forecasts are underpinned by fresh demand from central banks, which are expected to purchase around 710 tonnes a quarter in 2025, and by ETF inflows that have sharply gained momentum after three years of outflows, holdings are already near all-time highs and October alone added $8.2 billion. Economic and geopolitical uncertainty, lower yields, a weaker dollar, and de-dollarization efforts continue to be cited as positive drivers, while the main downside risk is that momentum stalls if the Federal Reserve holds interest rates steady or if the U.S. dollar remains stronger than expected.